Ratan Tata: India's Most Beloved Industrialist

He could have been a playboy heir. Instead, Ratan Tata spent five decades building India's most respected conglomerate into a global powerhouse — acquiring Jaguar Land Rover, Tetley Tea, and Corus Steel while maintaining a reputation for integrity that made him a national treasure. Then he died, and a billion people mourned.

View all stories about this mogul

🏛️ Chapter 1: Born into Legacy

Ratan Naval Tata was born on December 28, 1937, into the most famous industrial family in India. But being born a Tata was not the uncomplicated privilege it might sound like.

The Tata Group had been founded in 1868 by Jamsetji Tata, Ratan’s great-great-uncle, and had grown into India’s largest and most diversified conglomerate. By the time Ratan was born, Tata companies produced steel, operated hotels, generated electricity, and ran airlines. The Tata name was synonymous with Indian industry itself.

But Ratan’s childhood was marked not by privilege but by disruption. His parents — Naval Tata and Sonoo Tata (née Commisariat) — separated when Ratan was seven. In 1940s India, divorce was extraordinarily rare and deeply stigmatized. Ratan and his younger brother, Jimmy, were raised primarily by their grandmother, Lady Navajbai Tata, in the family’s mansion in Mumbai.

“I had a lonely childhood. My parents separated early. I was raised by my grandmother, who was wonderful but strict. I grew up in a big house that often felt empty.”

The loneliness shaped him. While other wealthy Indian sons embraced the social whirl of Mumbai’s elite, Ratan was reserved, introspective, and uncomfortable with attention. He was more interested in machines than people, more comfortable in a workshop than a ballroom.

He was sent to boarding schools — first in Mumbai, then at the prestigious Cathedral and John Connon School. He was a decent student but not exceptional. What he was, even as a teenager, was stubborn. When Ratan Tata decided something, he didn’t change his mind. This would prove to be both his greatest strength and his most exasperating quality.

After completing high school, he went to the United States — to Cornell University, where he studied architecture and structural engineering. At Cornell, Ratan discovered two things: a love of design and a love of independence. In America, he was just another student. Nobody cared that he was a Tata. Nobody treated him differently. For the first time in his life, he was judged purely on his own merits.

He loved it. And a part of him never wanted to go back.

🏗️ Chapter 2: The Reluctant Heir

After graduating from Cornell in 1962, Ratan Tata faced a choice: stay in America and build his own career, or return to India and join the family business.

He chose India. Not enthusiastically, but dutifully.

JRD Tata — Jehangir Ratanji Dadabhoy Tata, the legendary chairman of Tata Group — was Ratan’s uncle and mentor. JRD had run Tata Group since 1938 and was, by the early 1960s, one of the most respected business leaders in India. He was also a pilot (he had flown India’s first commercial flight in 1932), a philanthropist, and a man of enormous personal charm.

JRD saw something in Ratan — a quiet intensity, an engineering mind, a stubborn integrity — that he believed the group needed. He also saw that Ratan would have to prove himself. Being a Tata by birth was not enough.

Ratan started on the shop floor. Literally. His first job was shoveling limestone at Tata Steel’s plant in Jamshedpur. He worked alongside laborers, lived in modest company housing, and learned the steel business from the ground up.

“JRD told me that if I wanted to lead this company, I had to understand it. Not from a boardroom. From the factory floor. So I shoveled limestone. I operated machines. I got my hands dirty. It was the best education I ever received.”

Over the next two decades, Ratan moved through various Tata companies — Tata Steel, NELCO (an electronics company), Empress Mills (a textile company). At each stop, he tried to modernize operations, cut costs, and improve quality. At each stop, he ran into resistance from entrenched managers who resented a young Tata heir telling them how to run their businesses.

The results were mixed. NELCO showed improvement under Ratan’s leadership but was devastated by the economic downturn of the 1970s. Empress Mills struggled with labor problems and outdated technology. Ratan was learning, but he was also accumulating enemies — company bosses who saw him as a threat to their autonomy.

The Tata Group in this era was less a unified corporation and more a loose federation of independent companies. Each company had its own chairman, its own board, and its own culture. The group chairman had influence but not authority. Getting anything done required persuasion, not orders.

For a man like Ratan Tata — quiet, direct, impatient with politics — this was maddening.

👑 Chapter 3: The Coronation

On March 25, 1991, JRD Tata stepped down as chairman of Tata Sons — the holding company that controlled the Tata Group. His successor was Ratan Tata.

The appointment was controversial. Ratan was 53 years old and had spent three decades in the Tata system, but he had never run a major profit center. His track record at NELCO and Empress Mills was underwhelming. Several senior Tata executives — particularly Russi Mody at Tata Steel and Darbari Seth at Tata Chemicals — believed they were more qualified for the top job.

They were probably right, on paper. But JRD chose Ratan for reasons that transcended résumé accomplishments. He believed Ratan had the vision and the integrity to transform the Tata Group from a collection of Indian companies into a global conglomerate.

The timing was remarkable. India was on the verge of economic liberalization. The License Raj — the elaborate system of government permits and regulations that had controlled Indian business since independence — was about to be dismantled. For the first time in decades, Indian companies would be free to compete globally, attract foreign investment, and expand internationally.

Ratan Tata took over Tata Group at exactly the moment when India opened up to the world.

“When I became chairman, people expected me to be a caretaker — to manage what existed. I had no intention of being a caretaker. I intended to transform this company into something the world would have to take seriously.”

His first challenge was internal. The fiefdom chairmen — Mody, Seth, and others — resisted Ratan’s authority at every turn. They controlled their companies with the possessiveness of feudal lords and viewed the new group chairman as an interloper.

Ratan moved carefully but relentlessly. Over the next several years, he retired or replaced the fiefdom chairmen one by one. Each departure was accompanied by drama, lawsuits, and newspaper headlines. It was the ugliest internal battle in Indian corporate history.

But Ratan won. By the late 1990s, he had consolidated authority over the Tata Group and begun the transformation that would define his legacy.

🚗 Chapter 4: The Indica and the Nano

Ratan Tata loved cars. He had designed cars as a hobby at Cornell. He dreamed of building a car that ordinary Indians could afford.

In 1998, Tata Motors launched the Indica — India’s first indigenously designed and manufactured passenger car. It was a modest vehicle by global standards but a milestone for Indian industry. The Indica proved that India could design and build a car from scratch, without foreign partners or licensed technology.

The Indica was a commercial success. But Ratan Tata wasn’t satisfied. He wanted to go further — much further.

In 2003, at the Geneva Motor Show, Ratan saw entire Indian families — parents and multiple children — riding on a single scooter through Indian traffic. It was dangerous. It was common. And it was, Ratan decided, unacceptable.

He announced that Tata Motors would build a car for one lakh rupees — approximately $2,500 at the time. The world’s cheapest car. A “people’s car” that would give India’s growing middle class an affordable, safe alternative to the scooter.

“I saw families on scooters and I thought: these people deserve a car. Not a luxury car. Not even a good car. Just a car. Something with four wheels and a roof that keeps them safe.”

The Tata Nano launched in 2009 to enormous media attention. It was priced at 100,000 rupees as promised — an engineering marvel of cost reduction that required reinventing nearly every component of the automobile.

But the Nano was a commercial failure. Indian consumers didn’t want the world’s cheapest car — they wanted a car they could aspire to. The “cheapest car” label was a stigma, not a selling point. Sales were disappointing, and the Nano was eventually discontinued in 2018.

The Nano’s failure taught Ratan Tata an important lesson about markets and aspirations. Price isn’t everything. In a country where a car is a symbol of social progress, being associated with “cheap” was fatal.

But the Nano’s engineering innovations — in materials science, manufacturing efficiency, and cost optimization — would find their way into other Tata vehicles for years to come. Sometimes the lessons from failure are worth more than the failure costs.

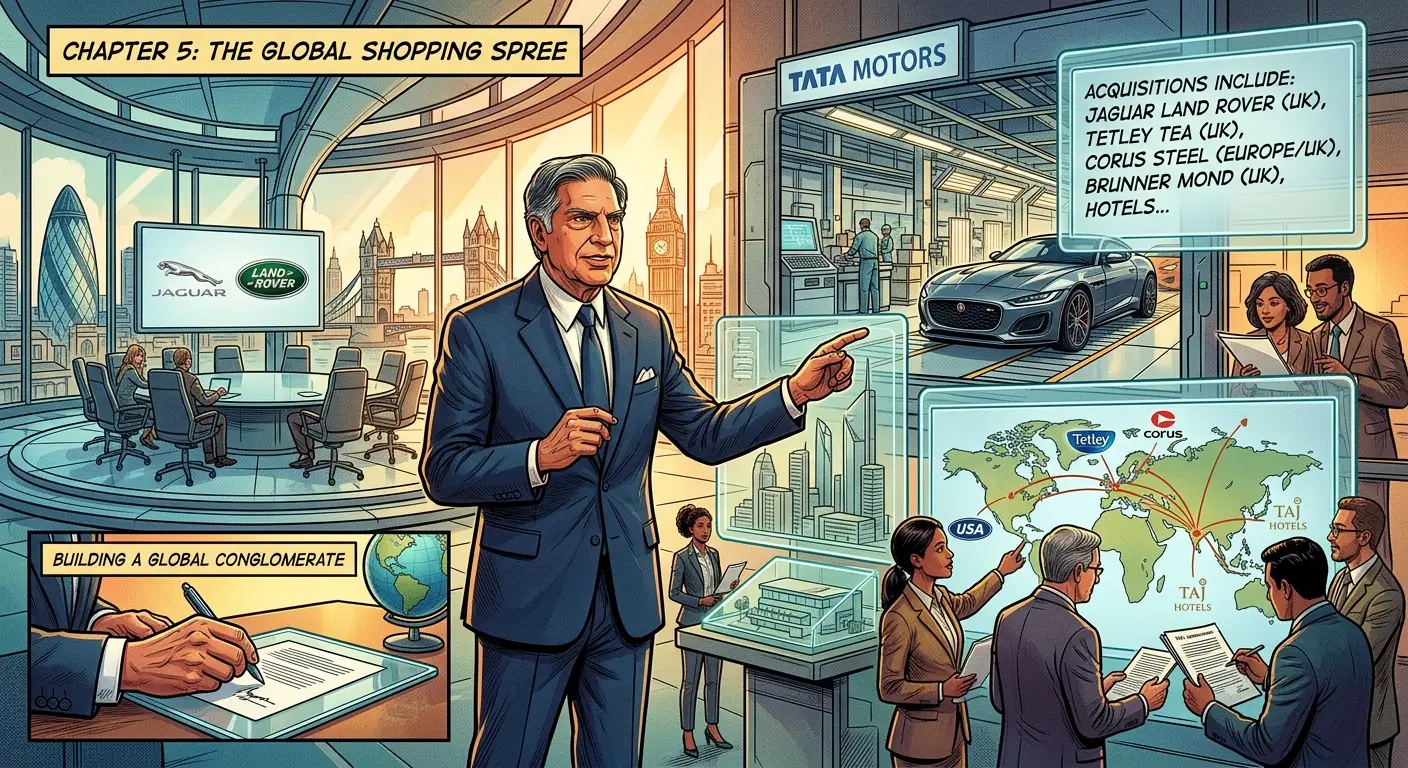

🌍 Chapter 5: The Global Shopping Spree

If the Nano represented Ratan Tata’s heart, his international acquisitions represented his strategic mind.

Between 2000 and 2008, Ratan Tata went on the most aggressive acquisition spree in Indian corporate history, buying iconic Western brands and transforming Tata from an Indian conglomerate into a global one.

2000: Tetley Tea — Tata Tea acquired Tetley, the British tea brand, for $450 million. It was the largest acquisition by an Indian company at the time. A former British colony’s company buying one of Britain’s most iconic tea brands was rich with historical irony that Ratan was too polite to point out.

2004: Daewoo Commercial Vehicle — Tata Motors acquired Daewoo’s truck division in South Korea for $102 million, gaining access to the Korean and Asian markets.

2007: Corus Steel — Tata Steel acquired Corus (formerly British Steel) for $12 billion. This was the largest acquisition by an Indian company in history. Tata, the Indian steel company, now owned the British steel company. The colonized had, quite literally, acquired the colonizer.

2008: Jaguar Land Rover — The crown jewel. Tata Motors acquired Jaguar and Land Rover from Ford Motor Company for $2.3 billion.

“When we acquired Jaguar and Land Rover, the British press asked: can an Indian company run British luxury brands? The answer was: better than the American company that just sold them to us.”

The Jaguar Land Rover acquisition was Ratan Tata’s masterpiece. Ford had badly mismanaged both brands, losing billions of dollars. Tata invested in new models, improved quality, and — critically — gave JLR’s British management team autonomy to run the business without interference from Mumbai.

The results were spectacular. JLR went from losing money under Ford to generating billions in profit under Tata. The Range Rover became one of the most desirable luxury SUVs in the world. The Jaguar F-Type became a critically acclaimed sports car. By the mid-2010s, JLR was generating more revenue than Tata Motors’ entire Indian operations.

💔 Chapter 6: The Mumbai Attacks

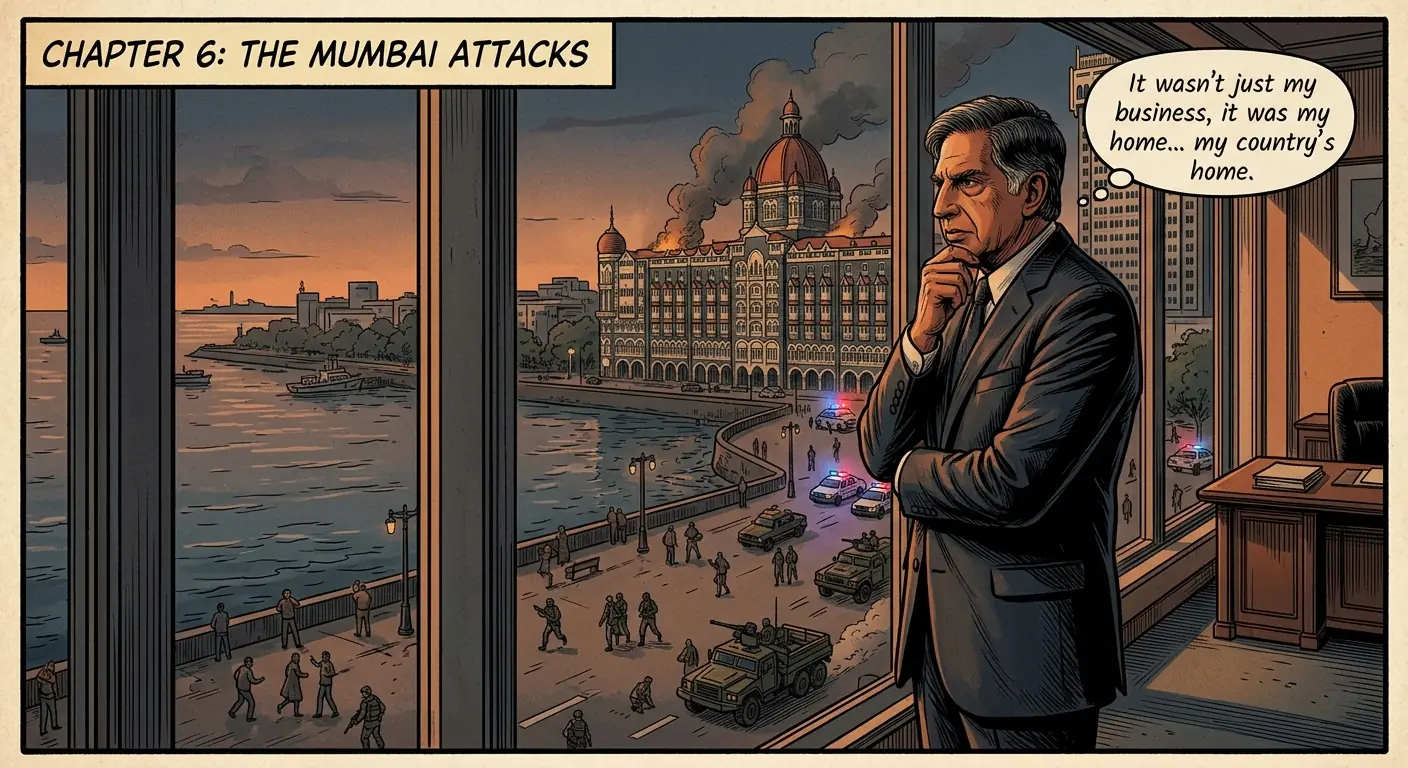

On November 26, 2008, ten terrorists from Pakistan attacked multiple locations in Mumbai, including the Taj Mahal Palace Hotel — the flagship property of the Tata Group’s hotel division, Indian Hotels Company.

The siege lasted three days. 166 people were killed, including 31 at the Taj hotel. The terrorists specifically targeted the hotel, knowing it was a symbol of Mumbai’s — and India’s — cosmopolitan aspirations.

What happened inside the Taj during the siege became legendary. Hotel staff — from the general manager to kitchen workers — risked their lives to protect guests. They formed human shields, led evacuations through service corridors, and refused to abandon their posts even as gunfire echoed through the halls. Eleven hotel employees were killed.

Ratan Tata’s response to the attacks defined his character. He personally visited the families of every employee who was killed. He established a fund to support the victims’ families — not just Tata employees, but all victims of the attacks. He committed to rebuilding the damaged sections of the hotel.

“The Taj is not just a hotel. It is a symbol of Mumbai, of India, of the idea that excellence can emerge from anywhere. The terrorists tried to destroy that idea. They failed. We will rebuild. And the Taj will be more beautiful than before.”

He was true to his word. The Taj was restored. The memorial to the fallen was built. The families were supported. And Ratan Tata’s reputation as a leader of profound decency was cemented.

In a country where corporate leaders were often viewed with suspicion, Ratan Tata was universally trusted. He wasn’t the richest business leader in India — not even close. The Ambani brothers, the Birlas, the Adanis — all had greater personal wealth. But none had Ratan Tata’s moral authority.

⚔️ Chapter 7: The Succession Wars

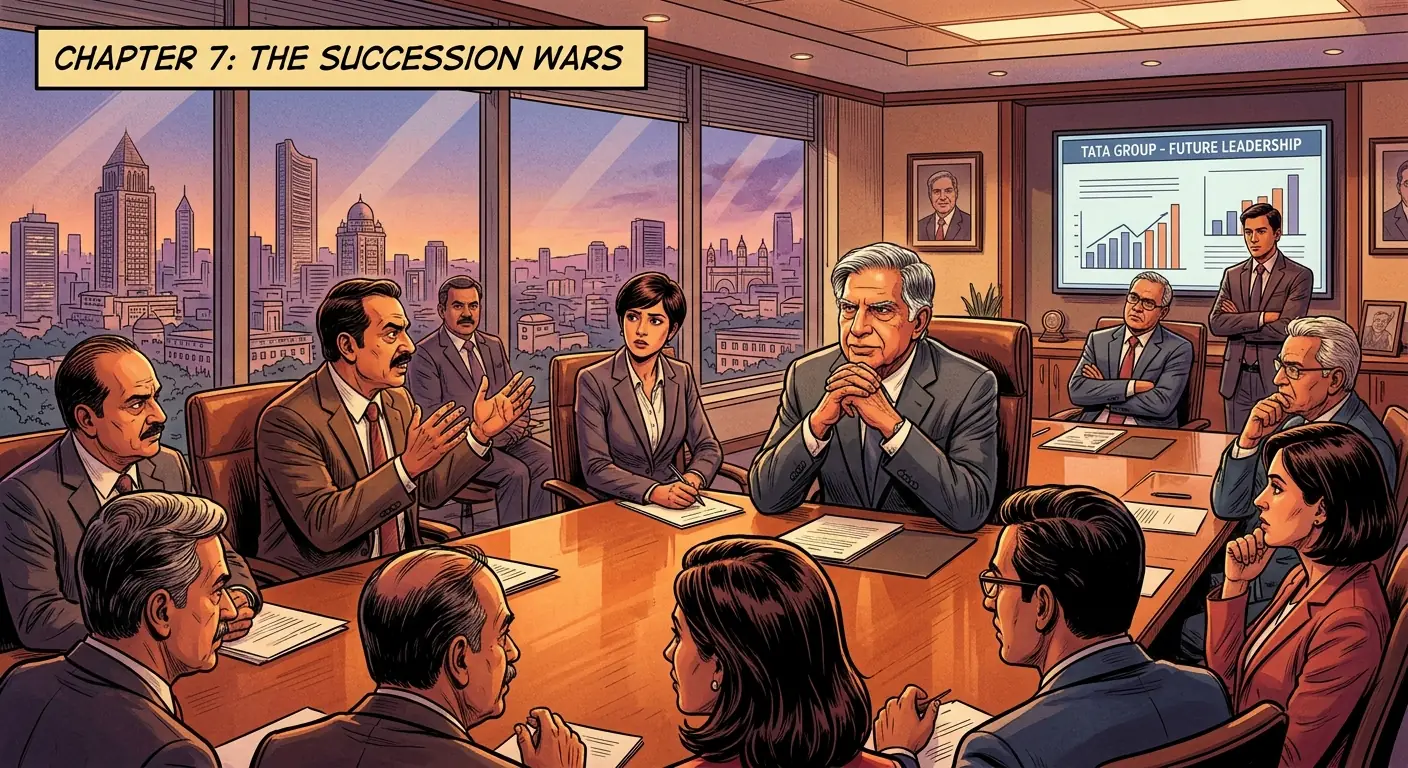

In December 2012, Ratan Tata retired as chairman of Tata Sons at the age of 75. His successor was Cyrus Mistry — a 44-year-old businessman from the Shapoorji Pallonji family, which held an 18.4% stake in Tata Sons.

The appointment of Mistry was itself controversial — many expected a Tata family member or a long-serving Tata executive to succeed Ratan. Mistry was an outsider, albeit one whose family had been major Tata shareholders for decades.

What followed was one of the most dramatic corporate power struggles in Asian business history.

Mistry took over and began making changes — some of which were genuinely needed and some of which alienated Tata Group’s old guard. He questioned the wisdom of certain Tata investments. He pushed for greater accountability. He challenged the autonomy of individual Tata company boards.

On October 24, 2016, the Tata Sons board fired Cyrus Mistry as chairman. The dismissal was sudden, shocking, and — according to Mistry — without warning or explanation.

Mistry fought back. He accused the Tata Trusts (controlled by Ratan Tata) of interfering in company management. He alleged that Ratan Tata had undermined him throughout his tenure. He filed legal challenges that would drag on for years.

“The Mistry affair was the ugliest episode in Tata Group’s history. It revealed that even India’s most respected company was not immune to the messy realities of corporate governance, family politics, and the difficulty of succession.”

Ratan Tata came out of retirement to serve as interim chairman while a search for Mistry’s replacement was conducted. In February 2017, N. Chandrasekaran — the CEO of Tata Consultancy Services — was appointed as the new chairman of Tata Sons.

Chandrasekaran proved to be an effective leader, stabilizing the group and refocusing on profitable growth. But the Mistry episode left scars. It raised questions about governance at Tata Sons that the group had never previously faced.

Cyrus Mistry died in a car accident on September 4, 2022, at the age of 54. The legal disputes between the Mistry family and Tata Group continued after his death.

🐕 Chapter 8: The Man Behind the Empire

Ratan Tata never married. He came close — reportedly engaging to a Los Angeles woman in the 1960s — but the relationship ended, reportedly because she was unwilling to move to India. He had other relationships over the decades, but none led to marriage.

He lived modestly by billionaire standards. He drove himself to work (in a Tata car, naturally). He lived in a relatively simple apartment in Mumbai, sharing it with his German Shepherd dogs. He was famous for his love of dogs — he once built a small shelter for stray dogs at the Bombay House (Tata Group’s headquarters) and personally fed them.

In his later years, Tata became active on social media — particularly Instagram, where he shared photos of his dogs, cars, and occasional business wisdom. He became something rare in Indian business: a tycoon who was genuinely liked by ordinary people.

“Ratan Tata was the rare businessman who was loved not for his wealth but for his character. Indians trusted him because he seemed incapable of dishonesty. In a country where business leaders were routinely accused of corruption, Tata was the exception that proved the rule.”

He also became an active angel investor, backing dozens of startups in India’s growing technology ecosystem. He invested in Ola (India’s Uber equivalent), Paytm (digital payments), Snapdeal (e-commerce), and many others. His investments were typically small — a few million dollars — but his endorsement was worth far more than the money. Having Ratan Tata as an investor was the ultimate stamp of credibility in Indian business.

🕊️ Chapter 9: The Final Chapter

On October 9, 2024, Ratan Naval Tata died in Mumbai at the age of 86.

India mourned like it had lost a family member.

The tributes came from everywhere — from the Prime Minister to the cricket captain, from tech billionaires to taxi drivers. The Indian government declared a day of national mourning. His funeral cortege passed through the streets of Mumbai, lined with hundreds of thousands of people who had come to pay their respects.

“When Ratan Tata died, India didn’t just lose a business leader. It lost a moral compass. In a world of billionaires who optimize for wealth, Tata optimized for trust. That’s why a billion people mourned.”

The outpouring was remarkable because Ratan Tata was not a politician, not a cricket star, not a Bollywood actor — the categories of Indian public figure that typically generate mass emotional responses. He was a businessman. An industrialist. And yet his death triggered a national grief that reflected something deeper: a sense that India had lost someone genuinely good.

The Tata Group he left behind was a $150 billion conglomerate with over 100 operating companies in more than 100 countries. Tata Consultancy Services (TCS) was one of the world’s largest IT services companies, with a market capitalization exceeding $150 billion. Tata Steel, Tata Motors, Tata Power, Taj Hotels, Titan Company, Voltas, Trent — the list of Tata companies read like a directory of Indian industry.

And 66% of the shares of Tata Sons — the holding company that controlled it all — were owned by Tata charitable trusts. The majority of the group’s profits flowed not to private shareholders but to philanthropy: education, healthcare, rural development, and the arts.

This structure — embedded by Jamsetji Tata and maintained by every subsequent chairman — meant that Tata Group was, in effect, a philanthropic enterprise that happened to run businesses, rather than a business that happened to do philanthropy.

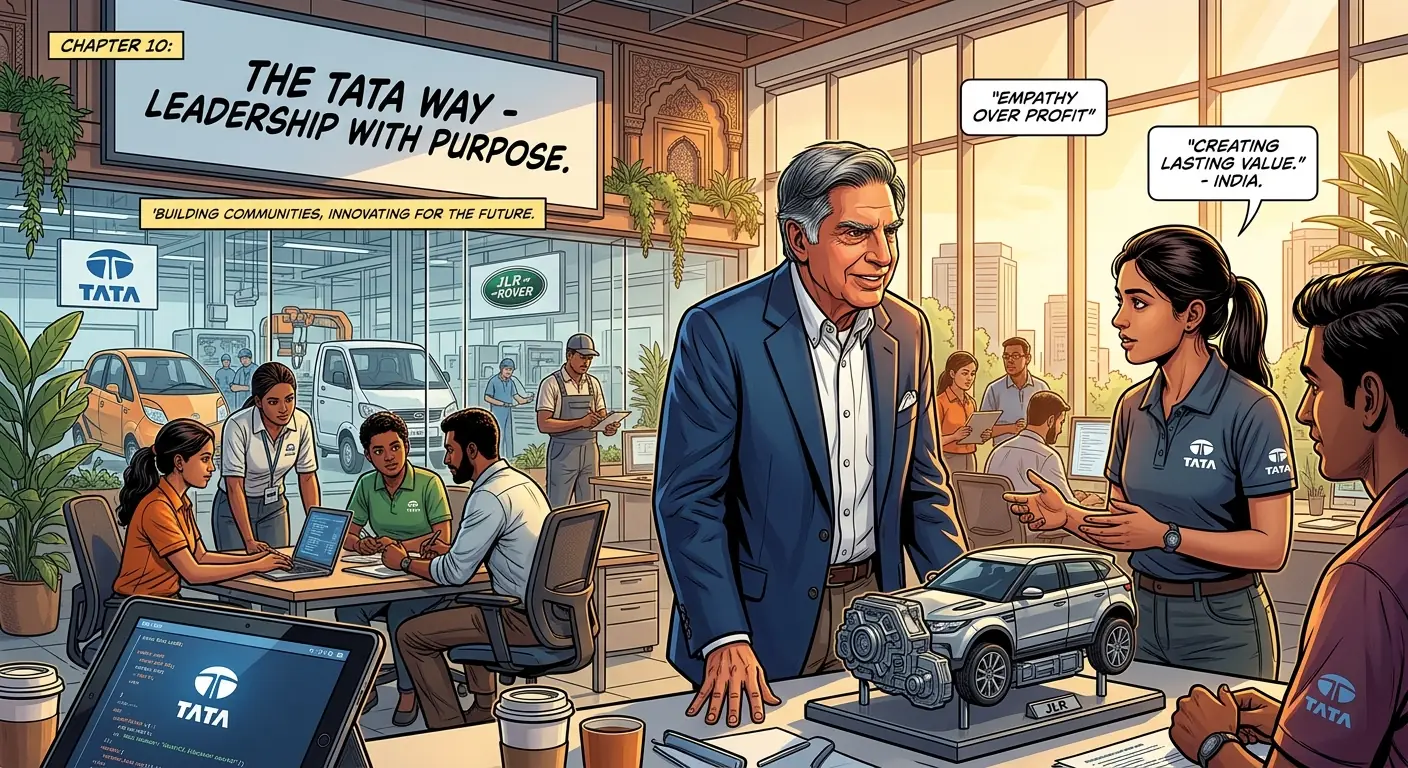

🏆 Chapter 10: The Tata Way

What can the world learn from Ratan Tata?

Lesson 1: Integrity is a business strategy.

In a business environment riddled with corruption, Tata’s reputation for honesty was a massive competitive advantage. Companies trusted Tata as a partner. Governments trusted Tata as an investor. Employees trusted Tata as an employer. Over decades, this trust compounded into something far more valuable than any financial metric.

Lesson 2: Think in centuries, not quarters.

The Tata Group was founded in 1868. Ratan Tata’s decisions were made with a 50-year horizon, not a 5-quarter one. The Jaguar Land Rover acquisition, the Corus Steel deal, the investments in startups — all made sense only if you were thinking in decades.

Lesson 3: The purpose of a business is not just profit.

Tata Group’s charitable trust structure proved that a company could be both profitable and purpose-driven. The trusts funded India’s premier research institutions (the Indian Institute of Science, the Tata Institute of Fundamental Research), hospitals, and educational programs.

Lesson 4: Quiet leadership is still leadership.

Ratan Tata was not charismatic in the traditional sense. He didn’t give rousing speeches. He didn’t dominate rooms with personality. He led through consistency, integrity, and an almost stubborn commitment to doing the right thing. In a world obsessed with loud leadership, his quiet example was revolutionary.

Lesson 5: Take care of people, and they’ll take care of the business.

The Taj hotel staff who sacrificed their lives during the Mumbai attacks didn’t do so because of a corporate policy. They did it because Tata Group had created a culture where employees felt genuinely valued and genuinely responsible. That culture was Ratan Tata’s greatest creation.

“What I want written on my tombstone is: ‘He made a difference.’ Not ‘He made money.’ Making money is easy. Making a difference is the hard part.”

Ratan Tata made a difference. For India. For the Tata Group. For the hundreds of millions of people whose lives were touched by Tata institutions, Tata hospitals, Tata schools, and Tata companies.

He was, in the end, exactly what India needed him to be: proof that you could build an empire without losing your soul.

The Tata Group’s combined revenue exceeds $150 billion as of 2025. Tata Consultancy Services has a market capitalization exceeding $150 billion. Approximately 66% of Tata Sons is owned by Tata charitable trusts, which fund education, healthcare, and development programs across India. Ratan Tata passed away on October 9, 2024.

🚀 Chapter 11: The Liberalization Leap (1991-Early 2000s)

When Ratan Tata took the helm in 1991, India was on the cusp of a seismic economic shift. The government, facing a balance of payments crisis, was forced to open up its socialist-leaning economy. Tariffs tumbled, licenses were abolished, and foreign competition was suddenly… a thing. For a sprawling, protected conglomerate like Tata, this was either an existential threat or the biggest opportunity in a century. Ratan chose opportunity, but not without a bloody fight.

Shedding the Old Skin: Modernizing the Conglomerate

India’s liberalization meant the end of the “License Raj,” a system where government permits dictated everything from production capacity to product lines. While many Indian companies, comfortable in their protected cocoons, quaked in their boots, Ratan Tata saw a chance to transform. The Tata Group, by 1991, was a diverse but often unwieldy beast, with over 300 companies and numerous “satraps” – powerful, often elderly, chairmen who ran their individual Tata companies like personal fiefdoms, largely independent of Bombay House (the Tata headquarters). This fragmented structure, once a strength, was now a liability.

Ratan embarked on a brutal, yet necessary, consolidation. He initiated a strategy to create a more unified, focused group, insisting that all companies bearing the Tata name contribute to a shared brand equity fee. This wasn’t just about money; it was about asserting central authority and a common vision. Many of the satraps resisted fiercely, having enjoyed decades of autonomy. It was a clash of titans, tradition versus transformation. Ratan, with his quiet but unyielding resolve, eventually won. He retired many of the old guard, streamlined operations, and pushed for professional management. It was a tough period, sometimes dubbed the “ratanisation” of Tata, marking a decisive break from the past.

Tech Visionary: Tata Consultancy Services (TCS) and Telecom

While the world was still figuring out this “internet thing,” Ratan Tata had a prescient vision for technology. He recognized early that India’s true global advantage lay not just in manufacturing, but in its intellectual capital. He poured resources into Tata Consultancy Services (TCS), which, under his tenure, blossomed from a domestic IT services provider into a global powerhouse. By 2004, TCS went public in India’s largest-ever IPO at the time, raising nearly $1.2 billion and cementing its status as a crown jewel of the Tata Group. It wasn’t just about software; Ratan also pushed hard into telecommunications. Tata Teleservices, launched in 1996, was an ambitious, capital-intensive venture into a nascent and highly competitive market. While it faced immense challenges and eventually saw a complex merger with Bharti Airtel, his early bet on these sectors fundamentally reshaped the Tata Group’s profile, moving it from purely heavy industry to a knowledge-economy leader.

Building a Global Mindset: Preparing for Expansion

Ratan Tata’s global ambitions weren’t just about buying iconic foreign brands later on. They were cultivated much earlier, during this liberalization phase. He understood that for Tata to compete on the world stage, it needed to think, act, and organize like a global entity. He pushed for international best practices, greater transparency, and a clear focus on shareholder value – concepts that were still relatively new in India. He encouraged Tata companies to seek out international partnerships and benchmarks, laying the groundwork for the audacious global acquisitions that would define the next decade. He was essentially telling a very Indian elephant, “Okay, time to learn to dance with the gazelles, and then perhaps buy a few.” His vision was clear: if India was opening up, Tata would not just survive, but thrive by becoming a truly global Indian enterprise.

💖 Chapter 12: The Quiet Philanthropist & Mentor (2010s-Present)

Even after stepping down as chairman of Tata Sons in 2012 (and then again, temporarily, in 2016), Ratan Tata didn’t exactly retreat to a quiet life of gardening and dog walks (though he certainly indulges in the latter). Instead, he seamlessly transitioned into the role of an elder statesman, a discerning investor, and perhaps most importantly, a mentor whose wisdom is sought by everyone from aspiring entrepreneurs to prime ministers. His post-retirement years have arguably illuminated the man behind the empire even more brightly, revealing a deep commitment to India’s future and a surprisingly sharp eye for disruptive innovation.

Investing in Tomorrow: Startup Ecosystem

Gone are the days of orchestrating multi-billion dollar acquisitions. Ratan Tata’s second act has been characterized by a different kind of investment: strategic, often personal, bets on India’s burgeoning startup ecosystem. Since 2014, he has invested his personal wealth (and time, which is arguably more valuable) in dozens of young companies, becoming one of India’s most prominent angel investors. From e-commerce giants like Snapdeal and Ola Cabs to payment platforms like Paytm, and even quirky ventures like DogSpot.in, his portfolio is incredibly diverse.

Why? It’s not just about financial returns, though he’s certainly made some shrewd calls. It’s about fostering innovation, supporting young Indian talent, and shaping the next generation of businesses. He often acts as an advisor, lending his immense credibility and network. “I see myself as a mentor,” he once remarked, “trying to help young people who have a dream.” His involvement often provides a crucial stamp of approval, opening doors for these startups that would otherwise remain firmly shut. It’s a pragmatic form of philanthropy, investing in job creation and economic growth one bold idea at a time. Who wouldn’t want Ratan Tata on their cap table? It’s like having Gandalf vouch for your startup.

Beyond the Boardroom: Advocacy and Advisory

Ratan Tata continues to serve as Chairman Emeritus of Tata Sons and holds positions on various international advisory boards, including those of JP Morgan Chase and Alcoa. He’s also a prominent voice on national policy, often advocating for ethical business practices, sustainable development, and improved infrastructure. His perspective, refined over decades of leading India’s largest conglomerate, carries immense weight. He’s often called upon to advise government committees, share insights at global forums, and lend his support to causes close to his heart.

His quiet influence extends to international relations too. His relationships with global leaders, built during his tenure as chairman, continue to serve as a bridge for India on the world stage. He embodies the idea of a “conscious capitalist,” believing that businesses have a responsibility beyond just profit – a philosophy deeply ingrained in the Tata Group’s DNA since Jamsetji Tata himself. He’s not just a businessman; he’s a national asset.

A Life Unmarried: His Personal Choices and Sacrifices

One aspect of Ratan Tata’s life that often sparks curiosity is his decision to remain unmarried. He has spoken about being “almost married four times,” each time stepping back due to circumstances or his intense commitment to the Tata Group. In a 2011 interview, he revealed that during his time in Los Angeles, he was in love and nearly settled down, but returned to India due to his grandmother’s illness. The subsequent 1962 Indo-China War made his intended partner’s family hesitant to move to India.

“I was in love with someone in America and we were very close to getting married. But I came back to India because my grandmother was unwell, and then, because of the Indo-China war, her parents didn’t want her to move to India. So, the relationship fell apart.”

This personal sacrifice, though perhaps not framed as such by him, speaks volumes about his dedication. His life has been inextricably linked with the Tata Group, a commitment that seemingly transcended personal relationships. It highlights the profound sense of duty that has defined him, perhaps making the Tata Group, in a very real sense, his truest family.

⚖️ Chapter 13: The Unsung Battles & Enduring Ethics (1990s-2010s)

While the Indica, Nano, and global acquisitions grab headlines, Ratan Tata’s tenure was also marked by less glamorous, but equally significant, battles. These weren’t just about market share; they were often about navigating India’s labyrinthine regulatory landscape, fending off fierce competition, and, crucially, upholding the Tata Group’s bedrock values in an environment often rife with temptation. The path to becoming India’s most respected industrialist wasn’t always smooth sailing; sometimes it was a full-blown brawl in the trenches, fought with integrity as his only shield.

The Telecom Tangle: Tata Teleservices’ Struggles and Scandals

Ratan Tata’s vision for telecommunications was bold, but the journey of Tata Teleservices (TTSL) was fraught with peril. Launched in 1996, it entered a cutthroat sector characterized by rapid technological change, intense price wars, and, unfortunately, significant regulatory ambiguity and even scandal. Unlike the success story of TCS, TTSL struggled for profitability for years, becoming a significant drain on the group’s resources. The biggest challenge came with the 2G spectrum allocation scam that rocked India in 2008-2011. While Tata was never directly implicated in the scam itself, the broader controversy and the subsequent policy paralysis created immense uncertainty for all telecom players.

TTSL’s partnership with Japan’s NTT DoCoMo, which invested $2.7 billion for a 26% stake in 2009, eventually soured. DoCoMo sought to exit in 2014 and demanded Tata buy back its shares at a pre-agreed price of ₹58 per share (approximately $0.95 at the time) – a total of about $1.17 billion. However, Indian regulations on foreign exchange prevented Tata from paying the full amount, leading to a bitter legal dispute in both Indian and international courts. Tata ultimately honored its commitment, securing a waiver from the Reserve Bank of India to pay DoCoMo $1.18 billion in 2017, a testament to Tata’s commitment to contractual obligations, even when it hurt. It was a costly lesson in navigating global partnerships within complex local regulatory frameworks, showcasing Ratan Tata’s unwavering commitment to the “Tata Way” of honoring commitments.

The Steel Wars: Competition and Consolidation

Tata Steel, the group’s oldest major enterprise, also faced its share of battles. While the 2007 acquisition of Corus was a triumph of global ambition, the pre-liberalization era saw it operate under the shadow of government control and then face new, aggressive domestic and international competitors. Ratan Tata oversaw the modernization and expansion of Tata Steel, ensuring it remained a formidable player. The late 1990s and early 2000s were a period of intense competition, with players like ArcelorMittal emerging as global giants. Tata Steel had to constantly innovate, improve efficiency, and expand its product portfolio to maintain its edge.

“We had to become lean, mean, and agile. The world had changed. You couldn’t just rely on history anymore.”

This meant tough decisions: shutting down inefficient plants, investing heavily in new technologies, and focusing on value-added products. Ratan Tata pushed for a culture of relentless improvement, ensuring that the legacy of Jamsetji Tata’s vision for steel continued to be relevant and competitive in a globalized world. It wasn’t just about making steel; it was about making better steel, more efficiently, and with a keen eye on environmental sustainability, long before it became fashionable.

Guardians of Trust: Upholding Tata’s Ethical Standards

Perhaps Ratan Tata’s most enduring, and often unsung, battle was the constant vigilance required to uphold the Tata Group’s legendary ethical standards. In a country where corruption and opaque dealings were, at times, distressingly common, Tata stood as an unyielding beacon of integrity. This wasn’t just a PR slogan; it was enforced. There are countless anecdotal stories, and some public instances, where Tata companies chose to walk away from lucrative deals rather than compromise on ethics.

For instance, Ratan Tata famously stated that Tata would never pay a bribe. This principle meant that sometimes the group lost out on projects to competitors who were less scrupulous. He instilled a culture where transparency and fair dealing were non-negotiable. This steadfast commitment to values, especially in challenging business environments, is arguably his most significant contribution to the Indian corporate landscape. It created a “trust premium” for the Tata brand, making it one of the most respected, not just in India, but globally. In an era where corporate scandals are depressingly common, Ratan Tata ensured that “Tata” remained synonymous with “trust.” And frankly, that’s a legacy worth more than any balance sheet could ever quantify.

💡 Key Insights

- ▸ Ratan Tata's approach to acquisitions was counterintuitive: he bought iconic Western brands (Jaguar, Land Rover, Tetley) not for their profitability but for their brand equity and technology. He was willing to overpay for acquisitions that gave Tata Group global credibility and manufacturing know-how. The lesson: sometimes the strategic value of an acquisition far exceeds its financial value, especially for companies trying to establish global legitimacy.

- ▸ The Tata Group's unique ownership structure — where 66% of the holding company is owned by charitable trusts — meant that the majority of Tata's profits flowed to philanthropy rather than to private shareholders. This structure gave Tata Group a social license to operate that competitors couldn't match and insulated it from the short-term pressures of public markets. Ratan Tata proved that doing good and doing well are not mutually exclusive — they can be structurally embedded in a company's DNA.