Vijay Mallya: The King of Good Times Who Ran Out of Time

He owned a Formula 1 team, a cricket franchise, and India's most glamorous airline. They called him the 'King of Good Times.' Then the debts came due, the banks came calling, and Vijay Mallya fled India with $1.4 billion in unpaid loans — becoming the most wanted fugitive in Indian business history.

View all stories about this mogul

🎉 Chapter 1: The Heir to the Party

Vijay Mallya was born to party.

Not metaphorically. Literally. His father, Vittal Mallya, was the chairman of United Breweries Group — India’s largest alcohol company, producer of Kingfisher beer, and the foundation of a business empire built on selling good times to a billion people.

Born on December 18, 1955, in Kolkata (then Calcutta), Vijay grew up in a world of privilege that few Indians could imagine. Private schools. European vacations. Exposure to business and politics from childhood. His father was a towering figure in Indian industry — a self-made billionaire who had built United Breweries from a regional brewer into a national powerhouse.

When Vittal Mallya died in 1983, Vijay inherited the chairmanship of UB Group at the age of 28. He was young, brash, and absolutely certain that he was destined for greatness.

“I didn’t inherit a company. I inherited a legacy. And I intended to make it bigger, bolder, and more spectacular than anything my father imagined.”

To his credit, the young Mallya did exactly that — at least for a while. He expanded UB Group aggressively, acquiring competitors, launching new brands, and turning Kingfisher beer into India’s most recognized alcohol brand. He diversified into real estate, fertilizers, and petrochemicals. By the 1990s, UB Group was one of India’s largest conglomerates, and Vijay Mallya was one of India’s most recognizable businessmen.

But it wasn’t just business that made Mallya famous. It was the lifestyle.

The yachts. The private jets. The parties on the French Riviera. The Kingfisher calendar featuring Bollywood actresses and international supermodels. The F1 team (Force India, later Racing Point). The IPL cricket team (Royal Challengers Bangalore). The racehorses. The vintage car collection.

Mallya didn’t just live large. He made living large into a brand strategy. Every yacht party, every calendar launch, every Grand Prix appearance was simultaneously personal indulgence and corporate marketing. Kingfisher wasn’t just a beer. It was a lifestyle. And Vijay Mallya was the lifestyle made flesh.

They called him the “King of Good Times” — a nickname he embraced with the enthusiasm of a man who had never considered the possibility that good times might end.

✈️ Chapter 2: The Airline Illusion

In 2005, Vijay Mallya launched Kingfisher Airlines.

If you’re thinking “a liquor mogul starting an airline sounds like a bad idea,” congratulations — you’re smarter than every banker who funded it.

Mallya’s vision was to create India’s most premium airline — a carrier that would offer luxury, service, and style that rivaled international carriers like Singapore Airlines and Emirates. Kingfisher Airlines would have beautiful flight attendants in designer uniforms, gourmet meals, personal entertainment systems, and the kind of attention to detail that Mallya brought to everything he touched.

The vision was seductive. The economics were suicidal.

“The Indian aviation market in 2005 was a graveyard for airlines. Low-fare carriers were driving down ticket prices. Fuel costs were rising. Airport infrastructure was inadequate. And Mallya chose this moment — this specific moment — to launch a premium, full-service airline. It was like opening a champagne bar in a recession.”

India’s aviation market was brutally competitive. Low-cost carriers like IndiGo and SpiceJet were winning market share by stripping costs to the bone and offering the lowest possible fares. Passengers, particularly domestic business travelers, cared about price and schedule — not luxury.

Mallya didn’t care. He was building a premium brand, and premium brands don’t compete on price. Kingfisher Airlines would charge premium fares for premium service. The Kingfisher brand — synonymous with good times and glamour — would differentiate the airline from its budget competitors.

It worked for about 18 months. Kingfisher Airlines launched to enthusiastic reviews. The service was genuinely excellent. The branding was immaculate. Load factors were respectable.

Then reality set in.

In 2007, Mallya acquired Air Deccan — a low-cost carrier — for approximately $300 million. The acquisition was supposed to give Kingfisher scale and access to Air Deccan’s route network. Instead, it gave Kingfisher a massive debt burden and the impossible challenge of integrating a budget airline with a premium one.

The Air Deccan acquisition doubled Kingfisher’s fleet and routes overnight. It also doubled its costs, its complexity, and its burn rate. The two airlines had different cultures, different service models, different labor agreements, and different customer expectations. Merging them was like trying to merge a five-star hotel with a youth hostel.

📉 Chapter 3: The Descent

From 2008 onward, Kingfisher Airlines was a money-losing machine of breathtaking efficiency.

The airline lost money in every single year of its existence. Cumulative losses exceeded $1.5 billion. The airline was burning through cash at a rate that required constant infusions from banks, from UB Group, and from Mallya’s personal resources.

The problems were structural and unfixable:

Operating costs were too high. Kingfisher’s premium service model required more staff, better meals, and more expensive equipment than its low-cost competitors. These costs couldn’t be reduced without destroying the brand.

Revenue was too low. Indian passengers weren’t willing to pay premium fares on domestic routes. Kingfisher’s load factors — the percentage of seats filled — consistently lagged competitors.

Fuel costs were rising. Aviation fuel accounted for 40-50% of operating costs, and prices spiked during the oil price surge of 2007-2008.

Debt was crushing. The Air Deccan acquisition had been funded primarily with borrowed money, and the interest burden was consuming whatever cash the airline generated.

“Kingfisher Airlines was losing approximately $1.5 million per day at its peak. Every day. The math was inescapable: unless something changed dramatically, the airline would run out of money. Nothing changed dramatically.”

Banks kept lending. This is the part of the story that mystifies observers. Why would Indian banks continue to extend credit to an airline that was clearly failing?

The answer involves politics, relationships, and the peculiar dynamics of Indian banking. Mallya was a member of the Rajya Sabha (India’s upper house of parliament). He was personally connected to senior politicians and bank executives. He was, in the Indian business hierarchy, too important to fail.

Indian public-sector banks — which were controlled by the government and managed by bureaucrats who were susceptible to political pressure — extended loan after loan to Kingfisher Airlines. The loans were restructured, extended, and forgiven. Collateral requirements were waived. Covenants were ignored.

By 2012, Kingfisher Airlines owed approximately $1.4 billion to a consortium of 17 banks. The airline had not turned a profit in a single year. Its fleet was grounded. Its license was suspended. Its employees hadn’t been paid in months.

Kingfisher Airlines was dead. But the debts lived on.

🏃 Chapter 4: The Flight

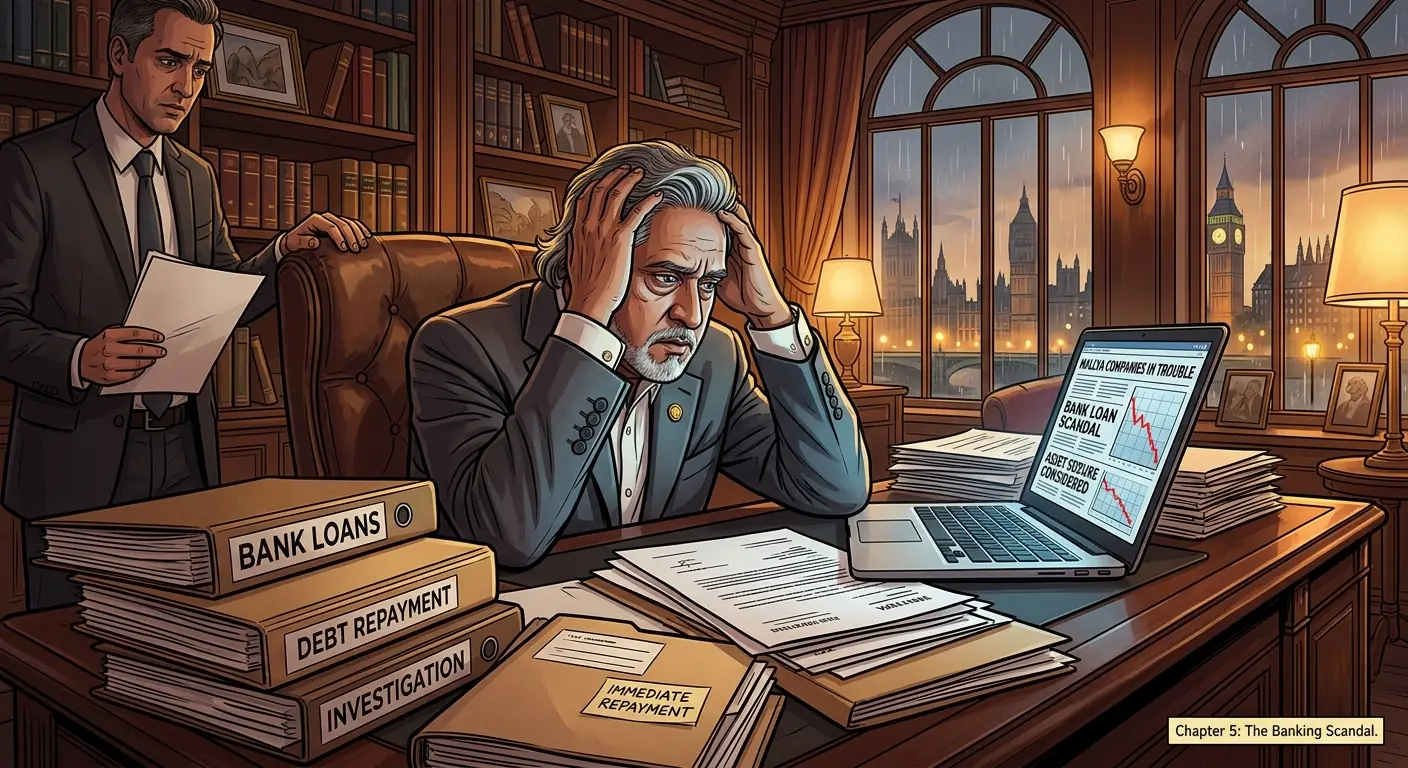

In March 2016, Vijay Mallya left India.

He claimed it was a business trip to England. Indian authorities believed it was a calculated escape from imminent arrest. The timing was suspicious: a consortium of banks had just obtained a debt recovery order against Mallya, and the Enforcement Directorate (India’s financial crimes agency) was closing in.

Mallya settled in England — specifically, in a luxury estate near Hertfordshire that he had purchased years earlier. He lived with his partner, a former Kingfisher calendar model, and maintained a lifestyle that seemed conspicuously extravagant for a man who owed $1.4 billion.

The Indian government was furious. Mallya was declared a “willful defaulter” — a legal designation indicating that he had the means to repay his loans but chose not to. The government initiated extradition proceedings through the British courts.

“The image was devastating: India’s most flamboyant billionaire, living in luxury in England, while the banks that had lent him $1.4 billion absorbed losses that were ultimately borne by Indian taxpayers. It became a symbol of everything wrong with India’s crony capitalist system.”

The extradition case dragged on for years. British courts examined whether Mallya would receive a fair trial in India, whether Indian prison conditions met European human rights standards, and whether the charges against him were politically motivated.

Mallya’s legal team argued that he was being persecuted for political reasons, that he had offered to repay the loans (an offer the banks rejected), and that the Indian justice system could not guarantee him a fair trial.

In 2020, a British court ruled that Mallya could be extradited to India. Mallya appealed. As of early 2026, the extradition process remained stalled in the British legal system, with Mallya continuing to live in England while Indian authorities continued to pursue him.

🏦 Chapter 5: The Banking Scandal

The Mallya saga exposed a rot at the heart of Indian banking that went far beyond one charismatic defaulter.

India’s public-sector banks — which controlled approximately 70% of the country’s banking assets — had been making politically influenced lending decisions for decades. Loans were extended not on the basis of creditworthiness but on the basis of connections. Industrialists with political ties received favorable terms. Risk assessment was cursory. Recovery was lax.

The result was a mountain of non-performing assets (NPAs) — bad loans that the banks had no realistic hope of recovering. By 2018, Indian banks’ NPAs exceeded $150 billion — approximately 10% of total loans.

Mallya’s $1.4 billion default was the most high-profile case, but it was far from the largest. Industrialists across India had borrowed billions from public-sector banks for projects that never materialized, businesses that never turned profitable, and lifestyles that were funded by debt.

“Mallya was the poster child, but he was not the disease. The disease was a banking system where loans were granted based on who you knew, not what you were worth. Mallya was just the most glamorous symptom.”

The Mallya case became a catalyst for reform. In 2016, India enacted the Insolvency and Bankruptcy Code (IBC) — a landmark law that created a time-bound process for resolving corporate insolvency. The IBC shifted power from defaulting borrowers (who had previously been able to stall recovery indefinitely) to creditors (who could now force asset sales through a structured process).

The IBC was one of the most significant economic reforms in modern Indian history. It didn’t solve the NPA problem overnight, but it fundamentally changed the incentive structure. For the first time, Indian borrowers faced real consequences for default.

🍺 Chapter 6: The Empire Unravels

While Mallya fought extradition in London, his business empire was being dismantled in India.

Banks seized and sold UB Group assets to recover their loans. Mallya’s shareholdings in United Spirits (the liquor subsidiary he had sold to Diageo in 2014 for approximately $3 billion) were attached by courts. His Indian properties — homes in Goa, Bangalore, and Mumbai — were confiscated.

Diageo, the British spirits giant that had bought United Spirits, pursued Mallya aggressively. In 2017, Diageo forced Mallya’s resignation from the United Spirits board and recovered approximately $75 million as part of a settlement.

The Force India F1 team — which had been a source of enormous personal pride for Mallya — was placed into administration in 2018. A consortium led by Lawrence Stroll acquired the team, which was renamed Racing Point and later became the Aston Martin F1 team.

The Royal Challengers Bangalore IPL team — another Mallya trophy asset — continued to operate under UB Group ownership but was increasingly distanced from Mallya personally.

“Everything Mallya built was taken away or sold off. The airline was gone. The F1 team was gone. The cricket team was distanced. The liquor empire was sold. All that remained was a fugitive in a Hertfordshire mansion and $1.4 billion in unpaid debts.”

By the mid-2020s, Mallya’s personal wealth — once estimated at over $1 billion — had been substantially diminished by legal costs, asset seizures, and the collapse of his business interests. He remained in England, technically free but practically imprisoned — unable to return to India without facing arrest, unable to travel to many countries that had extradition treaties with India, and unable to access assets that had been frozen by Indian courts.

🪞 Chapter 7: The Mirror

Vijay Mallya’s story is a mirror that reflects multiple truths simultaneously.

It reflects the failure of Indian banking governance. Banks that were supposed to serve the public interest instead served the interests of politically connected borrowers. The $1.4 billion lost on Kingfisher Airlines was ultimately borne by taxpayers and depositors — people who had no say in the lending decisions and no benefit from the airline’s existence.

It reflects the danger of brand overextension. The Kingfisher brand worked brilliantly for beer — a product associated with leisure, pleasure, and good times. It did not work for airlines — a business that requires operational discipline, cost control, and the willingness to make unglamorous decisions.

It reflects the seductiveness of lifestyle branding. Mallya’s personal brand — the yachts, the parties, the “King of Good Times” persona — was both his greatest marketing asset and his greatest liability. It attracted attention, created aspiration, and ultimately made his financial problems impossible to hide.

It reflects the limits of political protection. Mallya’s connections to Indian politicians protected him for years — keeping the loans flowing long after they should have stopped. But when public anger over his default became politically toxic, the same politicians who had enabled his borrowing were the first to demand his prosecution.

“Mallya is not a villain in the traditional sense. He’s something more complicated: a man who believed his own mythology. He convinced himself that the King of Good Times could not fail, that the party would never end, that the banks would always lend, and that the music would always play. He was wrong about all of it.”

🏆 Chapter 8: What Remains

Vijay Mallya turned 70 in 2025. He remained in England, living in reduced (but still comfortable) circumstances, fighting extradition, and maintaining — against all evidence — that he was innocent of wrongdoing and willing to repay his debts.

His story serves as a cautionary tale about leverage, ego, and the gap between lifestyle and substance.

The Mallya Lessons:

-

A good brand in one business is not a good brand in every business. Kingfisher was a great beer brand. Kingfisher Airlines was a $1.4 billion mistake. Brand extension requires understanding that different industries have different success factors.

-

Relationship banking is not the same as sound banking. When banks lend based on who you know rather than what you can repay, the result is predictable: massive defaults and systemic losses.

-

Lifestyle is not a strategy. Mallya’s extravagant lifestyle was great marketing for a liquor brand. It was terrible governance for an airline. The yachts and parties signaled that management was more focused on spending money than on making it.

-

When the math doesn’t work, charisma won’t save you. Kingfisher Airlines lost money every single year. No amount of brand power, political connection, or personal charm could change the fundamental economics.

-

Flight is not escape. Mallya left India to avoid arrest. But he traded Indian prosecution for British exile — unable to return home, unable to travel freely, and unable to rebuild. Sometimes the prison you choose is worse than the prison you’re avoiding.

The King of Good Times ran out of time. The party ended. The music stopped. And the bill, as it always does, came due.

Vijay Mallya remains in the United Kingdom as of 2026, fighting extradition to India. Indian courts have ordered the recovery of approximately $1.4 billion in defaulted loans. Kingfisher Airlines ceased operations in 2012 and had its license revoked in 2013.

🏏 Chapter 9: The Sports & Spectacle Show (2007-2016)

If there was one thing Vijay Mallya loved more than a good party, it was a good spectacle. And what better spectacle than the roaring engines of Formula 1 or the electrifying atmosphere of the Indian Premier League? For Mallya, sports weren’t just a pastime; they were a global billboard for his “good times” brand, Kingfisher, and an extension of his own larger-than-life persona. He didn’t just sponsor teams; he owned them, making sure his face was front and center, champagne bottle in hand, whenever a camera was near.

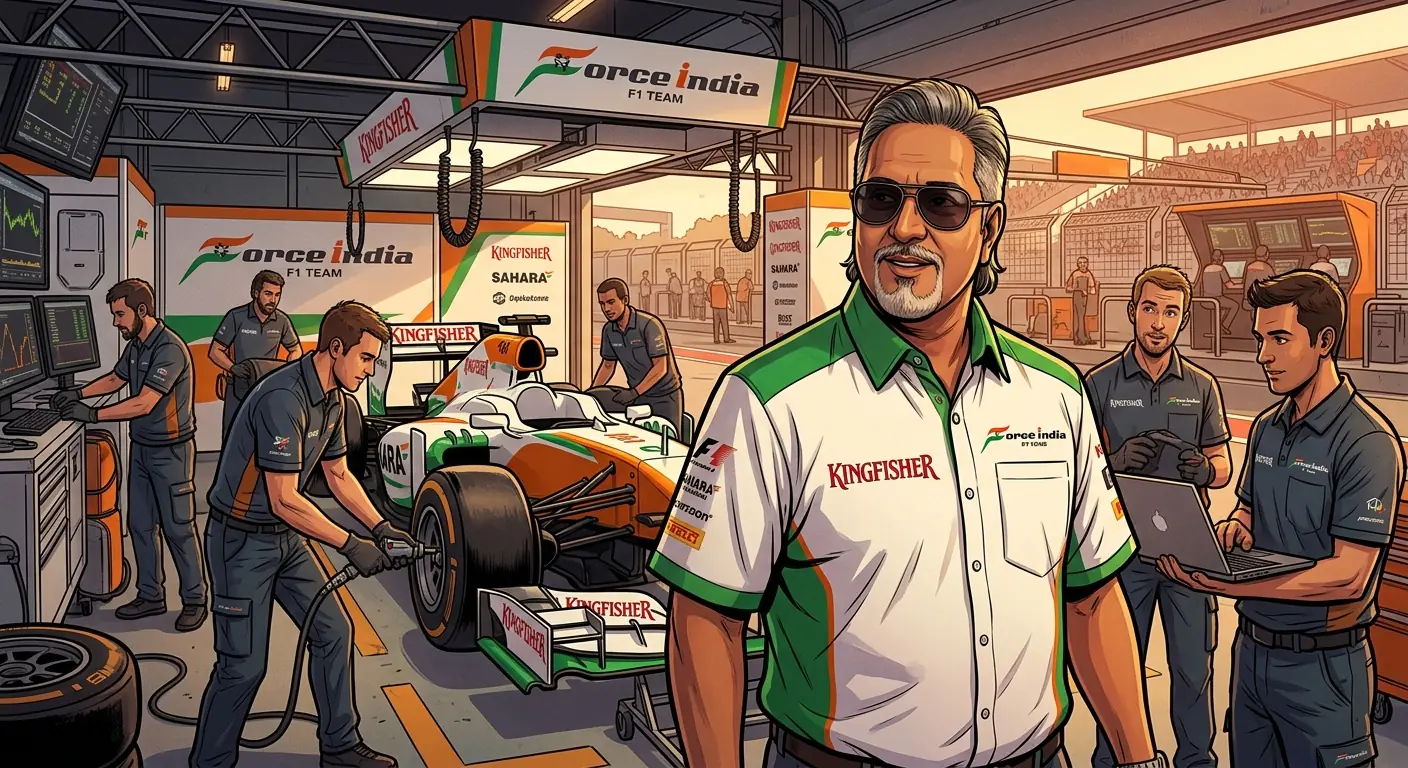

The Speed Demon’s Playground: Force India F1

In 2007, Mallya made a splash that reverberated through the highly exclusive world of Formula 1. He teamed up with Dutch entrepreneur Michiel Mol to acquire the struggling Spyker F1 team for a reported €90 million, which was roughly $120 million at the time. He swiftly rebranded it as Force India, proudly declaring it a team for a billion people. The vision was grand: an Indian team on the global stage of motorsport, draped in the tricolor, with Kingfisher logos plastered everywhere.

It was pure Mallya – audacious, ambitious, and financially precarious. F1 is a notorious money pit, even for the most well-funded constructors. While Force India had its moments of glory, scoring its first podium in 2009 and later becoming a consistent midfield contender, the financial drain was immense. Millions upon millions were poured into engine development, chassis design, and logistical nightmares. All this while Kingfisher Airlines was already hemorrhaging money back home. The irony was palpable: a luxury airline that couldn’t pay its fuel bills was bankrolling a Grand Prix team. It was like throwing a diamond party on a sinking ship.

Cricket’s Royal Challenger

The very next year, in 2008, Mallya doubled down on his sports obsession with the advent of the Indian Premier League (IPL). This Twenty20 cricket league was an instant sensation, merging India’s national religion with glitzy entertainment. Mallya, never one to miss a trend, successfully bid for the Bangalore franchise, Royal Challengers Bangalore (RCB), shelling out a staggering $111.6 million. This was the second-highest bid, only surpassed by Reliance Industries’ Mumbai Indians.

RCB quickly became another marquee platform for the Kingfisher brand. With star players like Virat Kohli, Chris Gayle, and AB de Villiers gracing the team, the Kingfisher logo was beamed into millions of homes, associated with thrilling victories (and sometimes, crushing defeats). Mallya reveled in the spotlight, often seen celebrating with players, embodying the spirit of celebration he wanted Kingfisher to represent. But much like Force India, RCB was more about brand visibility and personal passion than strict financial prudence. While the team generated revenue, it’s widely believed that the investment far outweighed the direct returns, particularly as the UB Group’s core businesses began to falter.

Beyond the Grandstands: A Collector’s Passion

Mallya’s love affair with sports wasn’t limited to these two giants. He had a deep, lifelong passion for horse racing, inheriting a stable of thoroughbreds from his father. He invested heavily, owning some of the finest horses in India, and the annual Kingfisher Derby was a social calendar highlight. He also briefly dabbled in Indian football, supporting storied clubs like East Bengal and Mohun Bagan. For Mallya, sports were a canvas for his dreams, a way to project an image of success, glamour, and unassailable good times. But beneath the glittering surface, these colossal investments were quietly siphoning off resources from an empire that was becoming increasingly fragile, laying bare the profound disconnect between Mallya’s extravagant public persona and his companies’ grim financial realities.

🏛️ Chapter 10: The Political Playbook (2002-2016)

For a man who seemingly valued champagne and supermodels above all else, Vijay Mallya had a surprising stint in the rather drab world of Indian politics. It wasn’t about public service, of course, but about power, access, and influence. Entering Parliament wasn’t just a vanity project; it was a strategic move that provided a crucial shield and opened doors that even his immense wealth couldn’t always pry open. Mallya’s foray into the Rajya Sabha, India’s upper house, illustrated a darker side of the nexus between big business and politics in India.

From Boardroom to Parliament

Mallya first got elected to the Rajya Sabha in 2002 as an independent member from his home state of Karnataka, with support from the Janata Dal (Secular) and the Congress party. He was re-elected in 2010, serving until 2016. Now, imagine this: the King of Good Times, with his extravagant lifestyle and jet-setting habits, sitting in the venerable halls of Parliament, theoretically representing the common man. It was a bizarre juxtaposition that few could reconcile.

His time in Parliament wasn’t marked by groundbreaking legislation or fiery speeches on behalf of the poor. Instead, it was about access. Being a Member of Parliament (MP) conferred a certain immunity, a direct line to ministers, and an undeniable aura of power. This position, critics allege, was used to secure favorable policies, expedite clearances, and, crucially, to delay any serious scrutiny into his increasingly precarious financial dealings. While Mallya often claimed his political role was to represent business interests, it’s clear the primary beneficiary was often himself and his struggling empire.

The Art of Influence

Mallya was a master networker. His parties were legendary not just for their opulence, but for the guest list that often included politicians from across the political spectrum, senior bureaucrats, and powerful industrialists. These were more than just social gatherings; they were strategic opportunities to cultivate relationships, exchange favors, and subtly exert influence. He understood that in India, personal connections often trumped formal processes.

Allegations of lobbying for Kingfisher Airlines were rife, particularly as the airline plunged deeper into debt. There were whispers of special dispensations, delayed tax payments, and lenient regulatory oversight. While concrete proof remains elusive in many instances, the perception was strong that Mallya’s political clout played a significant role in allowing Kingfisher Airlines to continue operating for far longer than it should have, despite its massive financial woes. The sheer number of banks, predominantly public sector, that continued to lend to a visibly failing enterprise, raised serious questions about whether political pressure was at play.

A Shield That Crumbled

For years, his political seat provided a useful buffer. Even as banks grew restless and employees went unpaid, Mallya remained largely untouchable. He attended parliamentary sessions sporadically, but his presence in the capital was a constant reminder of his influence. However, as the scale of Kingfisher Airlines’ default became undeniable and public anger surged, even his political shield began to crack.

In 2016, facing mounting pressure and the imminent threat of arrest, Mallya resigned from the Rajya Sabha via email, just days before the ethics committee was set to recommend his expulsion. His resignation was too little, too late. The shield had not just crumbled; it had been shattered by the weight of ₹9,000 crores (approximately $1.1 billion) in unpaid debts and the collective outrage of a nation. His flight to the UK shortly thereafter marked the definitive end of his political charade and the beginning of a relentless legal pursuit, underscoring that even the most well-connected individuals can eventually run out of political favors.

💸 Chapter 11: The Art of Debt-Fuelling (2009-2016)

Vijay Mallya wasn’t just the King of Good Times; for a significant period, he was the Emperor of Easy Credit. His empire, particularly Kingfisher Airlines, was largely fuelled by a staggering amount of debt, a house of cards built on optimistic projections, questionable collateral, and, quite possibly, a healthy dose of political influence. The story of how he managed to secure and then default on loans amounting to billions of dollars is a case study in corporate hubris and, arguably, systemic financial negligence.

The House of Cards: Kingfisher Airlines’ Debt

The numbers are eye-watering. By the time Kingfisher Airlines ceased operations in 2012, it owed a consortium of 17 Indian banks over ₹9,000 crores, which, depending on the exchange rate at the time of default, was well over $1 billion. The largest lender was the State Bank of India (SBI), followed by Punjab National Bank, IDBI Bank, and others. How did a single airline, consistently losing money, amass such a colossal debt?

Mallya’s strategy was simple, if ethically dubious: he leveraged the Kingfisher brand, shares of UB Group companies, and even personal guarantees to secure fresh loans. These funds were often used not to make the airline profitable, but to service existing debt – a classic “evergreening” tactic. When the airline needed a lifeline, Mallya would present a restructuring plan, promise a turnaround, and somehow convince banks to throw good money after bad. The underlying assets were often overvalued, and the Kingfisher brand, while potent for beer, proved a flimsy collateral for a failing airline. It was like mortgaging a castle made of candy floss.

The Banks’ Blind Eye (or Complicity?)

Perhaps the most perplexing question in this whole saga is: why did banks keep lending? Despite Kingfisher Airlines’ evident financial distress, its consistent losses, and its inability to pay employees or fuel suppliers, the credit lines kept flowing. Critics point to several factors. First, Mallya’s formidable political connections (as discussed in Chapter 10) may have put pressure on public sector banks to extend credit. Second, there was a perceived “too big to fail” mentality; banks worried that if Kingfisher collapsed, it would trigger a wider financial crisis, or at least a significant write-off on their books.

Third, there’s the uncomfortable truth about due diligence. Were these banks truly assessing the risks, or were they swayed by Mallya’s charisma and the perceived prestige of the Kingfisher brand? The sheer scale of the default eventually led the Central Bureau of Investigation (CBI) and the Enforcement Directorate (ED) to investigate allegations of a criminal conspiracy between Mallya and some bank officials. In 2016, Mallya was declared a “willful defaulter” by several banks, a designation for those who have the capacity to repay but refuse to do so. This wasn’t just a business failure; it was turning into a major financial scandal.

Asset Stripping and Diversion of Funds

As investigations deepened, more disturbing allegations surfaced. The ED, in particular, accused Mallya of diverting loan funds for purposes other than the airline’s operations. These funds allegedly went to his other companies, overseas accounts, and even for personal expenses, including the purchase of properties and the maintenance of his lavish lifestyle. For instance, an audit by SBI showed that ₹263 crores (approx. $35 million) were allegedly transferred to Force India F1 from Kingfisher Airlines between 2010 and 2012.

The legal battles that ensued involved frantic attempts by banks to recover their money by seizing and auctioning Mallya’s assets, both corporate and personal. From the Kingfisher Villa in Goa to shares in UB Group companies, everything became fair game. However, many assets were either already encumbered, overvalued, or simply difficult to liquidate. The debt-fuelling spree created a massive hole in the Indian banking system, making Mallya a symbol of corporate greed and the urgent need for stricter corporate governance and accountability. The ₹9,000 crores wasn’t just a number; it represented the collective savings of millions of Indian taxpayers, casually spent on a lifestyle that eventually imploded.

🥂 Chapter 12: Family, Feasts, and Frivolity (1980s-2016)

Behind the business acumen (or lack thereof, depending on who you ask) and the political maneuvering, there was Vijay Mallya the man – a man utterly consumed by the pursuit of pleasure and the maintenance of an extravagant, almost theatrical, lifestyle. His personal life, often lived as publicly as his business ventures, was a testament to unbridled indulgence. While his companies spiraled into debt, Mallya remained steadfast in his commitment to “good times,” for himself and his inner circle, blind to the impending storm.

A Tale of Two Marriages (and More)

Mallya’s personal relationships were as colorful as his shirts. He married Sameera Tyabjee, an air hostess, in the 1980s, and they had a son, Sidhartha Mallya. Their marriage, however, was short-lived. He later married Rekha Mallya, a childhood friend, who had two daughters from a previous marriage, Laila and Tanya, and with whom he had a third daughter. Rekha remained a constant presence by his side, often seen at his lavish parties and public appearances.

His son, Sidhartha, became a minor celebrity in his own right, often seen accompanying his father to F1 races and IPL matches, and later attempting a career in acting and modeling. Sidhartha’s social media presence, often showcasing a similarly privileged and carefree lifestyle, drew criticism as his father’s financial troubles mounted. For Mallya, his family was part of his personal brand – a beautiful, well-dressed entourage that underscored his image as a successful patriarch living life king-size. The stark contrast between this picture-perfect family life and the thousands of unpaid employees and creditors would later become a painful point of contention.

The Goa Villa: An Epitome of Excess

If there was one single property that symbolized Mallya’s unbridled excess, it was the legendary Kingfisher Villa in Candolim, Goa. Perched on a cliff overlooking the Arabian Sea, this sprawling property was not just a home; it was Mallya’s ultimate party pad, hosting the infamous Kingfisher Calendar launches and countless celebrity bashes. With infinity pools, sprawling lawns, and direct beach access, it was the epitome of luxury, a place where the “King of Good Times” reigned supreme.

The villa became a focal point of the debt recovery efforts. After Mallya fled, banks tried multiple times to auction it off, facing repeated failures due to its high reserve price and legal complexities. It was finally sold in 2017 to actor-businessman Sachiin Joshi for ₹73 crores (approximately $10 million at the time), significantly less than its perceived market value. The sale of the Kingfisher Villa wasn’t just a transaction; it was a powerful symbol of the downfall, a tangible representation of how the good times had indeed run out. Each failed auction was a public humiliation, and its eventual sale marked the beginning of the dismantling of his personal kingdom.

The Collector’s Obsession

Mallya’s indulgences extended far beyond parties and properties. He was a passionate collector, particularly of vintage cars. His collection, housed in various locations, boasted some of the rarest and most expensive automobiles in the world. He also owned a vast art collection, private jets (including an Airbus A319 with custom interiors), and multiple yachts. His famous yacht, the Indian Empress, was a floating palace with a crew of 30, a helipad, and a cinema.

This relentless acquisition of luxury goods continued even as Kingfisher Airlines was in its death throes, consuming vast sums of money that could have been used to pay off creditors or keep the airline afloat. It highlighted a profound disconnect: while thousands of employees lost their jobs and livelihoods, Mallya was still living a life of unimaginable opulence. His personal spending wasn’t just extravagant; it was, for many, an affront to decency, a clear indication that for Vijay Mallya, the “King of Good Times,” the party was always for an audience of one.

⚖️ Chapter 13: The Long Arm of the Law (2016-Present)

The party ended abruptly for Vijay Mallya when he boarded a flight to London in March 2016, leaving behind a trail of unpaid debts, angry banks, and a furious Indian public. His flight was not merely an escape; it ignited one of India’s most high-profile extradition battles, turning the “King of Good Times” into a symbol of economic offenders and a test case for India’s resolve to bring its fugitives to justice. The legal saga, still ongoing, is a complex web of international law, diplomatic efforts, and Mallya’s tenacious defense.

The Extradition Saga Begins

India formally submitted an extradition request to the United Kingdom in February 2017, accusing Mallya of fraud and money laundering related to the collapse of Kingfisher Airlines. The request led to his dramatic arrest in London in April 2017, though he was quickly granted bail. This marked the beginning of a protracted legal battle in the UK courts, where the Indian government, through the Crown Prosecution Service, had to present a prima facie case against him.

The core of India’s argument was that Mallya had deliberately misrepresented Kingfisher Airlines’ financial health to secure loans, knowing well that the airline was in dire straits, and then diverted those funds. Mallya, on the other hand, maintained that he was a victim of political persecution and a failed business venture, arguing that he had no intention to defraud and that the loans were legitimate business decisions that simply went awry. The world watched as the Westminster Magistrates’ Court began hearing evidence, scrutinizing every detail of Mallya’s financial dealings and the Indian banking system.

The UK Courts and Their Scrutiny

The extradition hearings were a grueling process, with Mallya’s legal team employing every possible argument to prevent his return. They raised concerns about the conditions of Indian jails (specifically Mumbai’s Arthur Road Jail), claiming they were not up to international standards. The Indian government responded with detailed assurances, even providing videos and blueprints of the specific cell where Mallya would be held, complete with medical facilities.

In a significant victory for India, District Judge Emma Arbuthnot ruled in December 2018 that Mallya had a case to answer, stating that there was “clear evidence of dispersal and misapplication of the funds” and that he had “misrepresented the true financial state of Kingfisher Airlines.” Mallya immediately appealed to the High Court in London, which upheld the extradition order in April 2020, dismissing his claims about poor jail conditions and the lack of a strong case against him. His final legal avenue in the UK, an application to appeal to the UK Supreme Court, was also rejected in May 2020, seemingly exhausting all his options.

The Unfinished Business: Legacy and Lessons

Despite the UK Supreme Court’s rejection, Mallya has yet to be extradited. He remains in the UK, reportedly exploring further legal avenues, including seeking asylum, though details remain opaque. The delays highlight the complexities of international law and the often frustrating pace of justice when dealing with high-profile individuals with substantial resources.

Mallya’s saga has left an indelible mark on India. It has spurred the government to enact tougher laws against economic offenders, like the Fugitive Economic Offenders Act of 2018, and has put immense pressure on banks to improve their due diligence and accountability. For the Indian public, Mallya has become a symbol of corporate greed and the frustration with a system that often seems to protect the powerful. His flight and subsequent legal battles have underscored the importance of ensuring that no one, regardless of their wealth or connections, is above the law. The “King of Good Times” may have run out of time, but his legacy continues to shape India’s fight against financial crime, serving as a cautionary tale of unchecked ambition and the devastating consequences of living a lie. His story, far from over, continues to be a powerful lesson in accountability.

💡 Key Insights

- ▸ Mallya's story illustrates how personal brand can become corporate liability. His 'King of Good Times' persona — the yachts, the parties, the supermodels — was brilliant marketing for a liquor empire. But when applied to an airline, it created unrealistic expectations, inflated costs, and a culture of extravagance that was incompatible with the razor-thin margins of the aviation business. The lesson: the brand that works in one industry can be fatal in another.

- ▸ The Indian banking system's willingness to extend and restructure Mallya's loans long after Kingfisher was clearly insolvent reveals the darker side of relationship-based banking. Banks lent to Mallya not because the loans were sound but because he was a powerful industrialist with political connections. The Mallya saga helped trigger India's Insolvency and Bankruptcy Code of 2016 — a landmark reform that fundamentally changed how Indian banks dealt with defaulting borrowers.