Warren Buffett: The Quiet Man Who Became the Greatest Investor Who Ever Lived

He bought his first stock at eleven, filed his first tax return at thirteen, got rejected by Harvard, and then spent seven decades turning a dying textile mill into a $900 billion empire — all from the same house he bought for $31,500 in 1958.

View all stories about this mogul

In 2008, while the global financial system was melting down and grown men on Wall Street were literally weeping at their desks, a seventy-eight-year-old man in Omaha, Nebraska, wrote an op-ed in the New York Times with the headline “Buy American. I Am.” He then proceeded to pour billions of dollars into the smoldering wreckage of the U.S. economy — Goldman Sachs, General Electric, Bank of America — while everyone else was running for the exits. Within a few years, those bets had made him richer by tens of billions of dollars.

That man still lives in the same house he bought in 1958 for $31,500. He eats McDonald’s for breakfast almost every morning. He drinks five Cherry Cokes a day. He drove himself to work in a Lincoln Town Car for decades. And as of 2026, at ninety-five years old, he is worth over $140 billion, commands a conglomerate valued at over $900 billion, and is widely regarded as the greatest investor who has ever lived.

This is the story of Warren Edward Buffett — how a weird, numbers-obsessed kid from Omaha became the Oracle, what his methods actually are, and why he still won’t retire.

🌱 Chapter 1: Omaha — A Boy Who Loved Numbers (1930–1947)

Warren Edward Buffett was born on August 30, 1930, in Omaha, Nebraska — right in the gut of the Great Depression. His father, Howard Buffett, was a stockbroker whose clients were getting annihilated by the worst market crash in American history. The timing was terrible for a stockbroker and perfect for shaping a future investor who would become pathologically obsessed with understanding risk.

Howard Buffett was a fascinating guy in his own right — deeply principled, politically engaged, and eventually elected to the U.S. Congress as a Republican representative from Nebraska. He was a strict fiscal conservative and a devotee of the gold standard, so opposed to deficit spending that he reportedly returned his congressional pay raise. Warren worshipped his father. Howard’s integrity, his intellectual independence, his refusal to follow the crowd — all of that seeped into Warren’s DNA.

His mother, Leila, was a different story. According to Alice Schroeder’s biography The Snowball, Leila had a volatile temper and could be emotionally cruel, particularly when Howard was away. Warren reportedly found refuge in numbers — they were predictable, logical, and they never yelled at you. Math became his sanctuary.

The Kid Who Counted Everything

From the moment Warren could think, he was counting things. License plates. Population figures from the World Almanac. The frequency of letters in newspaper articles. He didn’t just like numbers — he consumed them, the way other kids consumed comic books. His childhood friends later described him as a walking calculator who could do complex math in his head faster than most adults could do it on paper.

At age six, he bought a six-pack of Coca-Cola from his grandfather’s grocery store for twenty-five cents and sold each bottle for a nickel — a five-cent profit on a quarter invested. A 20% return. He was six years old, and he was already thinking about margins.

By age eleven, he bought his first stock: three shares of Cities Service Preferred, at $38 per share. He bought them for himself and three for his sister Doris. The stock promptly dropped to $27. His sister reminded him daily that he was losing her money. When it recovered to $40, he sold. The stock subsequently rocketed to $202.

That experience — selling too early, watching a stock quintuple after he’d bailed — burned itself into his brain like a brand. Decades later, he’d call it one of the three most important lessons of his life: be patient. The money is made in the waiting, not in the trading.

The Paper Route Empire

Most kids who deliver newspapers have one route. Warren had five. Simultaneously. He woke up before dawn, mapped out the most efficient delivery paths, and cleared over $175 a month — in the 1940s, that was more than most of his teachers were making. He filed his first tax return at age thirteen and, in a move that tells you everything about Warren Buffett, reportedly claimed his bicycle as a business deduction.

When his family moved to Washington, D.C. — Howard had won his congressional seat — Warren added a Washington Post route to his empire. He was literally delivering the newspaper he would one day save by investing $10 million in its parent company.

The Pinball Machine Scheme

At seventeen, Warren and his friend Don Danly bought a used pinball machine for $25 and installed it in a barbershop. The deal was simple: the barber got a cut, and Warren and Don kept the rest. The machine made so much money they bought more. Within months, they had a chain of pinball machines across Omaha. Warren eventually sold the business for $1,200.

He was a teenager running a passive income operation. Most seventeen-year-olds were worrying about prom. Warren was worrying about return on invested capital.

By the time he graduated high school, Warren had saved over $5,000 — roughly $67,000 in today’s dollars. He reportedly told a friend, “I’m going to be a millionaire by the time I’m thirty.” He wasn’t bragging. He was doing the math.

“I always knew I was going to be rich. I don’t think I ever doubted it for a minute.” — Warren Buffett

🎓 Chapter 2: The Education — Graham, Columbia, and the Intellectual Foundation (1947–1956)

Warren’s father wanted him to go to college. Warren wasn’t thrilled — he felt like he already knew more about money than most professors. He enrolled at the Wharton School at the University of Pennsylvania and spent two years being underwhelmed. He found the curriculum too theoretical, too detached from actual business. He transferred to the University of Nebraska, where he finished his undergraduate degree in three years total, graduating at nineteen.

Then came the rejection that changed his life.

Harvard Said No

Warren applied to Harvard Business School. He was nineteen, slight, baby-faced, and absolutely brimming with confidence about his money-making abilities. The admissions interviewer in Chicago took one look at him, spent about ten minutes asking questions, and rejected him. Warren was reportedly crushed.

But here’s the thing: Harvard rejecting Warren Buffett might be the most consequential admissions mistake in the history of higher education. Because that rejection forced Warren to look elsewhere — and he discovered that Benjamin Graham, the father of value investing and author of The Intelligent Investor and Security Analysis, was teaching at Columbia Business School.

Warren applied to Columbia immediately. He was accepted. And what happened next was like a key sliding into a lock.

The Gospel According to Graham

Benjamin Graham’s philosophy was deceptively simple: a stock is not a ticker symbol or a line on a chart. It’s a piece of a real business. Your job as an investor is to figure out what that business is actually worth — its intrinsic value — and then buy it only when the market is offering it for significantly less than that. The gap between price and value is your margin of safety. The bigger the gap, the better your protection against being wrong.

Graham had another concept that hit Warren like a thunderbolt: Mr. Market. Imagine, Graham said, that every day a manic-depressive business partner shows up at your door offering to buy your share of the business or sell you his. Some days Mr. Market is euphoric and quotes a ridiculously high price. Other days he’s terrified and will practically give his shares away. Your job isn’t to follow Mr. Market’s moods. Your job is to exploit them.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

Warren inhaled Graham’s teachings with the fervor of a religious convert. He was the only student in the history of Graham’s class to receive an A+. Graham later said Buffett was the best student he’d ever had.

Working for the Master

After Columbia, Warren desperately wanted to work for Graham. He offered to work for free. Graham said no — reportedly explaining that Wall Street firms in that era still had discriminatory hiring practices, and he preferred to reserve his positions for Jewish analysts who might face barriers elsewhere. Warren went back to Omaha and worked at his father’s brokerage, Buffett-Falk & Company, for a couple of years.

In 1954, Graham changed his mind and offered Warren a job at Graham-Newman Corp. in New York. Warren leapt. For two years, he worked directly under the greatest living practitioner of value investing, learning to analyze balance sheets, assess businesses, and — most importantly — to think independently. When the market was panicking, you were supposed to be buying. When it was euphoric, you were supposed to be selling. The crowd was almost always wrong at the extremes.

Graham retired in 1956 and offered to make Warren his successor. Warren said no. He was going back to Omaha. He was twenty-five years old, had about $174,000 in savings, and had an idea for how he was going to compound it into something enormous.

💼 Chapter 3: The Partnerships — Compounding at Thirty Percent (1956–1969)

On May 1, 1956, Warren Buffett started Buffett Partnership, Ltd. — and the first thing you should know is that he didn’t even have a proper office. He worked out of a bedroom in his house. He was twenty-five, had seven initial partners (including his sister Doris and his Aunt Alice), and a total starting capital of $105,100. His own contribution was just $100.

The rules were classic Buffett — simple, fair, and designed to align everyone’s incentives. He would take 25% of profits above a 6% annual return. If he lost money, he’d absorb the losses personally before his partners did. No management fee. No slick pitch deck. Just: give me your money, I’ll try to grow it, and I’ll eat my own cooking.

The Returns

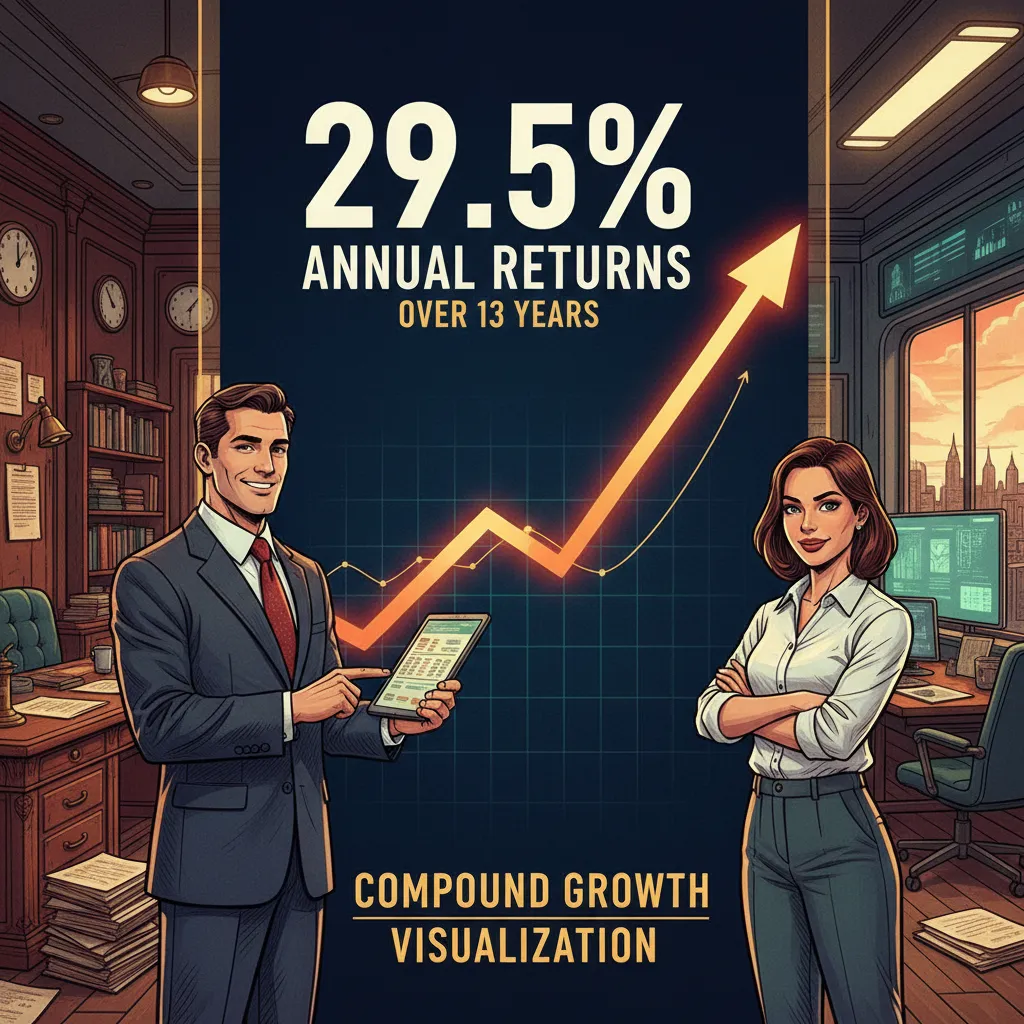

What happened next was one of the greatest runs in the history of finance. Over thirteen years, from 1957 to 1969, Buffett’s partnerships delivered a compounded annual return of 29.5% — before his cut. After his performance fee, his investors still earned about 23.8% annually. During the same period, the Dow Jones Industrial Average returned roughly 7.4% per year.

He never had a losing year. Not one. Across thirteen years that included recessions, market panics, and a presidential assassination. The Dow lost money in five of those thirteen years. Buffett made money in all thirteen.

His $105,100 starting pool grew to over $100 million by 1969. His personal wealth went from nearly nothing to about $25 million. He was thirty-nine years old. The promise he’d made as a teenager — millionaire by thirty — turned out to be wildly conservative. He was ahead of his own math.

How He Did It

Buffett’s early strategy was a mix of Graham-style deep value plays and a few special situations — what he called “workouts.” He’d find companies trading below their liquidation value (what the company would be worth if you sold all its assets and paid off its debts), buy as much as he could, and wait. Sometimes he’d buy enough stock to influence the company’s direction. Sometimes he’d just sit and let the market come to its senses.

A few of his best early investments:

- Sanborn Map Company — a mapmaking company whose investment portfolio was worth more than its entire stock price. Buffett bought enough shares to join the board and forced a reorganization that unlocked the hidden value.

- Dempster Mill Manufacturing — a windmill maker in Beatrice, Nebraska. Buffett bought a controlling stake, installed new management, and turned it around.

- American Express — after the company’s stock cratered during the 1963 “Salad Oil Scandal,” Buffett bet big, buying 5% of the company when everyone else was running. He reportedly spent time at restaurants and shops observing whether people were still using their American Express cards. They were. The stock recovered spectacularly.

That American Express investment marked a subtle but critical evolution in Buffett’s thinking. Graham had taught him to buy cheap assets — companies trading below the value of their tangible stuff. But American Express wasn’t cheap on the balance sheet. It was cheap relative to the power of its brand. People trusted the green card. That trust was worth billions, but it didn’t show up on any spreadsheet. Buffett was starting to think about intangible value — the power of brands, customer loyalty, and competitive moats. This evolution would eventually transform him from a very good investor into the greatest one who ever lived.

Shutting It Down

In 1969, at the peak of his powers and in one of the greatest winning streaks in financial history, Buffett did something nobody expected: he closed the partnerships and returned everyone’s money.

Why? Because he couldn’t find cheap stocks anymore. The market was overheated, speculative, and — in his judgment — dangerous. Rather than compromise his standards or risk his partners’ capital in a frothy market, he simply walked away.

“I am not attuned to this market environment, and I don’t want to spoil a decent record by trying to play a game I don’t understand just so I can go out a hero.” — Warren Buffett, 1969 letter to partners

The market crashed shortly after. Buffett’s timing, as usual, was impeccable.

He suggested his partners invest with two people: either Bill Ruane (who went on to run the legendary Sequoia Fund) or a guy named Charlie Munger. Remember that name.

🏭 Chapter 4: Berkshire Hathaway — The Textile Mill That Ate the World (1965–1985)

The story of how Warren Buffett came to own Berkshire Hathaway is one of the strangest origin stories in business — because he’s said repeatedly that buying it was the worst investment he ever made.

Berkshire Hathaway was a struggling textile manufacturer in New Bedford, Massachusetts. By the early 1960s, the company was a classic Graham-style cigar butt — a mediocre business trading below its book value, with just a few puffs left. Buffett started buying shares in 1962 at around $7.50 per share.

The CEO, Seabury Stanton, periodically offered to buy Buffett’s shares back through tender offers. In 1964, Stanton and Buffett verbally agreed on a tender price. Then the formal offer came in — an eighth of a point lower than what they’d agreed to.

Buffett was furious. Not because the money mattered — it was a trivial amount. He was angry about the principle. Stanton had tried to shortchange him. So instead of selling, Buffett did the opposite: he bought more shares, took control of the company, fired Stanton, and became chairman of a dying textile mill.

He later called it “the dumbest stock I ever bought.” He estimated that buying Berkshire — and trying to save its textile operations — cost him roughly $200 billion in opportunity cost compared to if he’d just put that capital into good businesses from the start. Two hundred billion dollars. Because a guy tried to stiff him on an eighth of a point. Buffett has a sense of humor about it. Mostly.

The Transformation

But here’s where the genius kicked in. Buffett couldn’t save the textile business — cheap foreign competition was killing New England textiles, and no amount of brilliant management could change that. So instead of fighting a losing war, he used Berkshire as a holding company — a vehicle to buy and hold other businesses and investments.

The first major acquisition was National Indemnity, an insurance company in Omaha, bought in 1967 for $8.6 million. Insurance turned out to be the perfect business for Buffett, and not for the obvious reasons.

The Float

Here’s the key: insurance companies collect premiums upfront and pay claims later. The money sitting between premium collection and claim payment is called the “float.” It’s not your money — technically it belongs to future claimants — but you get to invest it in the meantime. For free.

Buffett realized that if you ran insurance companies well — if you were disciplined about underwriting and didn’t write stupid policies — the float was essentially a permanent, interest-free loan that kept growing as you wrote more policies. You could use it to buy stocks, bonds, and entire companies.

As of 2025, Berkshire Hathaway’s insurance float stands at over $170 billion. That’s $170 billion of other people’s money that Buffett gets to invest at zero cost. It’s the financial equivalent of a perpetual motion machine. No other investor in history has had access to anything like it, and it’s the single biggest structural advantage behind Berkshire’s extraordinary returns.

See’s Candies and the Education of Warren Buffett

In 1972, Buffett and his partner Charlie Munger bought See’s Candies for $25 million. At the time, it felt expensive — Buffett was paying more than three times book value, which violated every Graham principle he’d been raised on. But Munger pushed him to see what Graham’s framework missed: See’s Candies had something magical.

The brand was beloved. Customers didn’t just like See’s — they loved it. And they’d pay premium prices because of that love. See’s could raise prices every year and nobody blinked. The company required almost no additional capital to grow. It was a cash machine — pouring profits directly into Berkshire’s coffers year after year.

See’s Candies taught Buffett the single most important lesson of his post-Graham evolution: it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

That one sentence changed his entire approach. From then on, he stopped looking for cheap cigar butts and started hunting for extraordinary businesses with durable competitive advantages — companies with what he’d come to call “moats.”

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” — Warren Buffett

See’s Candies cost $25 million in 1972. As of 2025, it has generated over $2 billion in cumulative pre-tax profits for Berkshire. Not bad for a candy shop.

🤝 Chapter 5: Charlie Munger — The Partnership That Changed Everything

You literally cannot tell the Warren Buffett story without talking about Charlie Munger. If Buffett is the greatest investor who ever lived, Munger was the guy who made him even better.

Charles Thomas Munger was born in Omaha in 1924, grew up six blocks from Buffett’s childhood home (though they didn’t meet as kids), attended Harvard Law School, and became a successful lawyer and real estate investor in Los Angeles. In 1959, a mutual friend introduced them at a dinner. The connection was immediate and electric.

Munger was everything Buffett wasn’t: a lawyer by training, a voracious reader across every discipline (physics, psychology, biology, history), sharp-tongued, and blunt to the point of being abrasive. Where Buffett was folksy and warm, Munger was acidic and cutting. Where Buffett worried about looking foolish, Munger didn’t care one bit.

Their first meeting, reportedly, lasted hours. According to Schroeder’s The Snowball, when friends later asked Munger about it, he said something to the effect of: “He’s going to be a very rich man.” When Buffett was asked about Munger, he reportedly said something similar.

”I’m Already a Little Bit Rich”

When Buffett tried to recruit Munger to leave law and go full-time into investing, Munger reportedly told him, in so many words: “I’m already a little bit rich. I’ll get there in my own time.” And he did — running his own investment partnership from 1962 to 1975 with returns that rivaled Buffett’s own.

They formally joined forces in the 1970s. Munger became vice chairman of Berkshire Hathaway in 1978, and for the next forty-five years, they sat side by side at every annual meeting, finished each other’s thoughts, and made one of the most consequential partnerships in business history.

Munger’s biggest contribution? He pushed Buffett beyond Graham’s strict value framework. Graham taught Buffett to buy cheap. Munger taught him to buy great. Quality businesses. Durable brands. Competitive moats that could withstand decades of assault. The See’s Candies acquisition was the first fruit of Munger’s influence. Coca-Cola, Apple, and dozens of other Berkshire mega-winners followed the same logic.

The Dynamic

At annual meetings, the two of them would sit on stage for six hours answering shareholder questions, and the dynamic was pure comedy. Buffett would give a detailed, thoughtful, fifteen-minute answer to a question. Then the moderator would turn to Munger. And Munger would say: “I have nothing to add.” Or: “That’s right.” Or, if he was feeling verbose: “Warren’s right, and it’s even more obvious than he made it sound.”

Other times, Munger would cut loose with a razor-wire observation that left the audience howling. On investment bankers: “I’d rather throw a viper down my shirt than hire a consultant.” On cryptocurrency: “I think the whole damn development is disgusting and contrary to the interests of civilization.” On the secret to a good marriage: “Lower your expectations.”

“All I want to know is where I’m going to die, so I’ll never go there.” — Charlie Munger

Munger passed away on November 28, 2023, at age ninety-nine — thirty-three days before his hundredth birthday. Buffett called him the “architect of Berkshire Hathaway” and said that without Munger, Berkshire would never have become what it is. The greatest investor in history is telling you that his partner made him better. Believe him.

🏰 Chapter 6: The Big Bets — Coca-Cola, Apple, and the Art of the Moat (1988–Present)

Buffett’s investment track record at Berkshire is one of the most remarkable documents in the history of capitalism. From 1965 to 2024, Berkshire Hathaway’s per-share market value increased at a compounded annual rate of approximately 19.8% — compared to about 10.2% for the S&P 500 including dividends. That doesn’t sound like much until you do the math: $1,000 invested in Berkshire in 1965 would be worth well over $40 million today. The same $1,000 in the S&P 500? About $300,000. Both are good. One is otherworldly.

Here are the bets that built the legend.

GEICO

Buffett’s relationship with GEICO spans his entire career. He first learned about the company as a twenty-year-old student, when he discovered that his hero Benjamin Graham sat on GEICO’s board. In 1951, on a Saturday, Buffett took the train to Washington, D.C., showed up at GEICO’s headquarters, and banged on the door until a janitor let him in. He found Lorimer Davidson, a GEICO executive, and talked his ear off for four hours about the insurance business.

Buffett bought GEICO stock immediately. Sold it a year later for a 50% profit. Then, in 1976, when GEICO was on the brink of bankruptcy — losing money on bad underwriting and trading at $2 a share — Buffett loaded up, eventually investing $46 million. In 1996, Berkshire bought the rest of GEICO outright for $2.3 billion. Today, GEICO is one of the largest auto insurers in the United States and a cornerstone of Berkshire’s insurance float.

Coca-Cola

In 1988, Buffett started buying Coca-Cola stock — eventually spending about $1.3 billion to acquire roughly 7% of the company. At the time, some people thought he was crazy. The stock wasn’t “cheap” by traditional value metrics. But Buffett saw what Graham’s framework couldn’t quantify: the most recognized brand on the planet, a product consumed 2.8 billion times per day in virtually every country on Earth, and a business model that printed cash with almost no capital expenditure required.

As of 2025, Berkshire’s Coca-Cola position, still virtually unchanged from the original purchase, is worth over $25 billion and generates roughly $750 million per year in dividends alone. The original investment has been paid back many times over in dividends alone, and the stock is still there, still compounding. Buffett has said he will never sell a single share.

This is the distilled essence of Buffett’s philosophy: find a business so good that you never have to think about it again. Buy it. Hold it. Collect the dividends. Go drink a Cherry Coke.

Apple

And then there’s Apple — the investment that even Buffett didn’t see coming.

Buffett famously avoided technology stocks for decades. He said tech was outside his “circle of competence” — the set of businesses he understood deeply enough to value with confidence. He watched the entire dot-com boom from the sidelines. He sat out Google, Facebook, and Amazon. The tech world considered him a dinosaur. He didn’t care.

Then, in 2016, Berkshire started buying Apple. Not because Buffett suddenly understood semiconductors or software engineering. He understood something simpler: Apple was no longer primarily a tech company. It was a consumer products company with the most loyal customer base on Earth. People didn’t just buy iPhones — they lived inside the Apple ecosystem and never left. That’s a moat.

Berkshire accumulated roughly $36 billion worth of Apple stock between 2016 and 2018. At its peak, that position swelled to over $170 billion, making Apple by far the largest holding in Berkshire’s portfolio — nearly half of its total equity investments. In 2024, Buffett began trimming the position, selling roughly half, reportedly citing concerns about future tax rates. Even after selling, Apple remained Berkshire’s largest stock holding.

The Apple investment added more to Berkshire’s net worth than almost everything else Buffett had done in the previous two decades combined. The man who avoided tech for forty years made what might be his single best investment ever — in a tech company. Sometimes being late to the party doesn’t matter if you bring the biggest check.

Other Greatest Hits

Buffett’s portfolio reads like a hall of fame of American capitalism:

- American Express — first bought during the Salad Oil Scandal of 1963, held ever since

- Bank of America — Buffett invested $5 billion in preferred stock during the 2011 financial crisis, later converted to common shares worth far more

- The Washington Post — bought in 1973 for $10 million, eventually worth over $1 billion

- Wells Fargo — a major holding for decades, though Buffett eventually exited entirely after the fake accounts scandal

- Dairy Queen — bought in 1998 for $585 million because Buffett liked the Blizzards

- BNSF Railway — Berkshire bought the entire railroad in 2010 for $44 billion, one of the largest acquisitions in American history

“Be fearful when others are greedy, and greedy when others are fearful.” — Warren Buffett

🏠 Chapter 7: The Personal Life — Cherry Cokes, McDonald’s, and the Unconventional Marriage

Warren Buffett is worth over $140 billion and lives in a gray stucco house in central Omaha that he bought in 1958 for $31,500. Adjusted for inflation, that’s about $330,000 in today’s dollars. It has five bedrooms, a decent yard, and no gate, no guardhouse, and — for most of his life — no security detail. His neighbors are regular people. He has lived there for nearly seven decades.

This isn’t some billionaire performance of humility. By all accounts, Warren genuinely doesn’t care about luxury. He doesn’t own a yacht. For decades, he didn’t own a vacation home. He has said that the house “has everything I need” and that living there makes him happy, so why would he leave?

The $3.17 Breakfast

Every morning, Buffett reportedly drives himself to McDonald’s. His order depends on how the market is doing. According to the HBO documentary Becoming Warren Buffett, when stocks are down, he goes cheap — a $2.61 sausage McMuffin. When things are okay, he upgrades to a $3.17 sausage McMuffin with egg. When the market is really rocking, he splurges on the bacon, egg, and cheese biscuit.

He uses coupons. The man is worth nine figures and he clips coupons for McDonald’s. A friend once reportedly watched him pay for lunch with a coupon, looked at him, and said, “Warren, you’re the richest man in the world.” Buffett reportedly responded: “That’s how you get to be the richest man in the world.”

He drinks approximately five twelve-ounce Cherry Cokes a day. He has said, apparently without irony, that he’s “about one-quarter Coca-Cola” and that since the mortality rate for all humans is eventually 100% regardless of diet, he’d rather enjoy what he eats. His daily caloric intake reportedly resembles that of a twelve-year-old boy at a birthday party: Coke, burgers, ice cream, steaks, and hash browns. His doctor once suggested he eat more broccoli. It reportedly did not go well.

The Marriages

Buffett’s personal life is more complicated than his folksy image suggests. He married Susan Thompson in 1952. By all accounts, Susie was warm, empathetic, socially gifted, and emotionally sophisticated in ways that Warren — who has described himself as “emotionally tone-deaf” — was not. She essentially taught him how to relate to other human beings.

In 1977, Susan moved to San Francisco to pursue a singing career. They never divorced. Instead, Susan introduced Warren to Astrid Menks, a Latvian-born waitress at a cocktail lounge that Warren frequented. Astrid moved in with Warren. Susan approved. For the next twenty-seven years, the three of them maintained what appeared to be an entirely amicable, unconventional arrangement. Holiday cards were signed “Warren, Susie, and Astrid.”

Susan Buffett died of cancer in 2004. Warren, reportedly devastated, married Astrid Menks in 2006 in a small ceremony. They remain married. The whole arrangement was — by Midwestern standards of the 1970s through 2000s — profoundly weird, and Buffett has never seemed remotely bothered by how it looked to anyone else.

The Flip Phone

For years, Buffett famously used a flip phone. Not a smartphone. Not even a basic smartphone. A flip phone — the kind of device most people’s grandparents had reluctantly upgraded from by 2010. He finally switched to an iPhone around 2020, reportedly at the urging of Tim Cook, who may have had a slight vested interest in the upgrade given that Berkshire owned about 6% of Apple at the time.

Buffett’s relationship with technology is, to be generous, cautious. He doesn’t use a computer to pick stocks. He doesn’t have email alerts for market movements. He reads annual reports, 10-K filings, newspapers, and trade publications — on paper, in many cases — and he makes decisions based on his understanding of the business, not the blinking of a screen.

“I don’t look at what the market is doing. I look at what the business is doing.” — Warren Buffett

🎪 Chapter 8: The Annual Meeting — Woodstock for Capitalists

Every year on the first Saturday in May, something strange happens in Omaha, Nebraska. Approximately 40,000 people — from investment professionals to retirees to college students to families — descend on the CHI Health Center arena for the Berkshire Hathaway annual shareholder meeting. Buffett himself dubbed it “Woodstock for Capitalists,” and the name stuck because it’s weirdly accurate.

The meeting is unlike any corporate event on Earth. There’s a massive exhibition hall where Berkshire’s subsidiaries set up booths — you can buy GEICO insurance, See’s Candies, Dairy Queen Blizzards, Brooks running shoes, and Ginsu knives, all under one roof. There’s a newspaper-throwing contest (Buffett’s childhood paper route lives on). There’s a 5K run. There’s a shopping day where Berkshire products are sold at discounts.

But the main event is the Q&A. Buffett and (until 2023) Munger sat on stage and answered shareholder questions for approximately six hours straight. No script. No teleprompter. No PR handlers feeding them talking points. Just two old guys with microphones, a box of See’s peanut brittle, cans of Cherry Coke, and a willingness to discuss absolutely anything.

The questions range from deeply technical (“What’s your current thinking on insurance reserve adequacy?”) to deeply personal (“How do you deal with loss?”) to deeply weird (“If you were a tree, what kind of tree would you be?”). Buffett answers all of them — with humor, with candor, and with an uncanny ability to reduce complex ideas to language a teenager could understand.

The Annual Letter

Buffett’s annual shareholder letter is one of the most widely read documents in finance. He’s been writing it since 1965, and over six decades, it has become a masterclass in business writing — folksy, funny, self-deprecating, and brutally honest about both successes and failures.

When Berkshire loses money on an investment, Buffett doesn’t hide behind euphemisms. He calls himself an idiot. When Berkshire’s textile operations kept hemorrhaging cash, he wrote: “I ignored Comte’s advice — ‘the intellect should be the servant of the heart, but not its slave’ — and so kept the operation alive far longer than I should have.” When Dexter Shoe Company — which he bought for $433 million in Berkshire stock — turned out to be worthless, he called it “the worst deal I’ve made” and flagged that paying in stock made the error doubly catastrophic.

Most CEO letters are ghostwritten corporate pablum designed to say nothing while appearing to say something. Buffett’s letters are the opposite — a billionaire talking to his partners like a friend explaining his thinking over a kitchen table. That honesty, sustained over sixty years, is a big reason why Berkshire’s shareholders trust him more than practically any CEO in history.

“Someone’s sitting in the shade today because someone planted a tree a long time ago.” — Warren Buffett

🎯 Chapter 9: The Philosophy — Moats, Circles, and the Art of Doing Nothing

If you distill Buffett’s investment philosophy to its essential elements, you get a framework so simple it almost seems like it shouldn’t work. And yet it has outperformed virtually every professional investor, algorithm, and hedge fund for over six decades. Here are the core principles.

Circle of Competence

Buffett insists that every investor — every person — has a circle of competence: a set of subjects they genuinely understand deeply. The key isn’t making your circle bigger (though that helps). The key is knowing exactly where the edge is and never stepping outside it.

This is why Buffett avoided tech stocks for decades. Not because he thought tech was bad. Because he knew he didn’t understand the dynamics well enough to bet billions on them with confidence. He’d rather miss a hundred winners outside his circle than lose money on one bad bet inside someone else’s.

Economic Moats

Buffett wants to own businesses with durable competitive advantages — what he calls “moats.” A moat is anything that protects a business from competition: a beloved brand (Coca-Cola), switching costs so high that customers can’t leave (Apple’s ecosystem), a cost structure so low nobody can undercut you (GEICO), network effects that grow stronger as more people join, or regulatory barriers that keep competitors out.

The moat metaphor is powerful because it emphasizes durability. Any company can have a good year. Buffett wants companies that can have a good century. The wider the moat, the longer the castle is safe.

Mr. Market and Temperament

From Graham, Buffett inherited the concept of Mr. Market — and he weaponized it. The stock market, Buffett argues, is there to serve you, not to instruct you. When Mr. Market offers you an amazing business at a stupid price because everyone is panicking, you should buy. When he offers you a mediocre business at an insane price because everyone is euphoric, you should sell — or, better yet, do nothing.

The crucial insight: investing is not an IQ test. It’s a temperament test. The market is full of brilliant people who consistently lose money because they can’t control their emotions. Fear and greed override their analysis. Buffett’s edge isn’t that he’s smarter than everyone else (though he’s very smart). His edge is that he doesn’t panic, doesn’t follow the crowd, and has the patience to sit on his hands for years when there’s nothing worth buying.

The Power of Doing Nothing

This might be the most counterintuitive element of Buffett’s philosophy: his best action, most of the time, is inaction. He buys a great business and then does absolutely nothing with it — for years, for decades, forever if possible. Berkshire has held Coca-Cola since 1988. American Express since the 1990s. His ideal holding period, as he’s famously said, is “forever.”

In a world where hedge funds trade millions of shares per second, where CNBC screams about market movements every fifteen minutes, and where apps let you buy and sell stocks while sitting on the toilet, Buffett’s approach — buy, hold, read, think, wait — is almost absurdly anachronistic. And it has beaten almost all of them.

“The stock market is a no-called-strike game. You don’t have to swing at everything — you can wait for your pitch.” — Warren Buffett

The $1 Million Bet

In 2007, Buffett made a public bet — $1 million — that a simple S&P 500 index fund would outperform a basket of hedge funds over ten years. The hedge fund industry, with its sky-high fees (typically 2% of assets plus 20% of profits), its legions of PhDs, and its sophisticated algorithms, couldn’t beat a boring index fund that charged almost nothing in fees.

Only one hedge fund manager, Ted Seides of Protégé Partners, took the bet. Over the next decade, the S&P 500 index fund returned 125.8%. Seides’s basket of hedge funds returned about 36%. It wasn’t even close.

Buffett’s point wasn’t that hedge fund managers are stupid. It was that their fees eat the returns alive. After you pay 2-and-20, even good performance becomes mediocre performance. For the vast majority of investors, a low-cost index fund is all you need. The Oracle of Omaha — a man who actively picks stocks for a living — is telling you that most people shouldn’t try to pick stocks. If that isn’t intellectual honesty, nothing is.

⚠️ Chapter 10: Controversies — The Oracle Isn’t Perfect

Buffett’s folksy persona and extraordinary track record have earned him a level of public trust that no other businessman in America enjoys. But that doesn’t mean he’s been right about everything, or that his hands are entirely clean.

Wells Fargo

Buffett was one of Wells Fargo’s biggest and most vocal supporters for decades. Berkshire was the bank’s largest shareholder. Even after the fake accounts scandal broke in 2016 — Wells Fargo employees, under intense pressure to meet sales quotas, had opened millions of accounts in customers’ names without their knowledge or consent — Buffett was slow to criticize. He defended the bank’s fundamental business and called the scandal a failure of management, not of the underlying model.

Critics saw this differently: a billionaire defending his investment while millions of ordinary customers got screwed. Buffett eventually sold Berkshire’s entire Wells Fargo position by 2022, but the episode dented his reputation as a values-driven investor.

Kraft Heinz

In 2015, Berkshire partnered with the Brazilian private equity firm 3G Capital to merge Kraft Foods and H.J. Heinz Company. The deal was supposed to create a packaged food behemoth. Instead, it became one of Buffett’s most visible failures.

3G’s playbook — aggressive cost-cutting, zero-based budgeting, and efficiency above all else — clashed with Buffett’s usual philosophy of buying great businesses and leaving them alone. Consumer tastes shifted away from processed food. Kraft Heinz wrote down $15.4 billion in impaired assets in 2019. The stock cratered. The SEC investigated accounting practices.

Buffett acknowledged the mistake: “I was wrong in a couple of ways about Kraft Heinz.” He admitted he’d overpaid for Kraft and that 3G’s cost-cutting model, while effective in some contexts, had its limits when applied to consumer brands that needed investment in innovation and marketing.

Too Slow on Tech

For years, the biggest knock on Buffett was that he missed the entire technology revolution. He sat out Microsoft despite being close friends with Bill Gates (who’s been on Berkshire’s board). He sat out Google. He sat out Amazon — and he’s said publicly that he was an “idiot” not to buy it, given that he understood and admired what Jeff Bezos was building.

His Apple investment partially redeemed this track record, but the critique isn’t wrong: Buffett’s circle-of-competence discipline, while protecting him from tech busts, also cost him enormous gains. The trade-off between caution and opportunity is real, even for the greatest investor who ever lived.

Succession Questions

For years, Berkshire watchers worried about what happens when Buffett is no longer running the show. The company’s culture, its decentralized management structure, and its capital allocation decisions all flow from one ninety-five-year-old man’s judgment. In recent years, Buffett has designated Greg Abel, the vice chairman overseeing non-insurance operations, as his successor. Whether Abel — or anyone — can replicate Buffett’s magic remains one of the great open questions in business.

🎁 Chapter 11: The Giving Pledge — Donating 99% of Everything

In 2006, Warren Buffett announced the most extraordinary act of philanthropy in history: he would give away approximately 99% of his wealth, primarily to the Bill & Melinda Gates Foundation, with the remainder going to foundations run by his three children — Susan, Howard, and Peter.

The initial pledge was staggering: he committed to donating roughly $37 billion in Berkshire Hathaway stock — at the time, the largest charitable gift ever made. He has continued donating billions in Berkshire shares every year since, and as of 2025, his total lifetime giving has surpassed $55 billion.

Why the Gates Foundation?

Buffett’s reasoning was characteristically practical. He didn’t want to build his own foundation from scratch. He didn’t want his name on buildings. He wanted his money to go where it would do the most good, deployed by people who knew what they were doing. Bill and Melinda Gates, he concluded, had built the world’s most effective philanthropic organization. So he gave them most of his fortune and said: “You’re better at this than I would be. Go.”

It was a strikingly un-egotistical move for a man who’s spent his entire life being right about capital allocation. Most billionaires who give big want their name in lights. Buffett essentially said: “Here’s $55 billion. Put it where it’ll save the most lives. Don’t worry about the credit.”

The Giving Pledge

In 2010, Buffett and Gates co-founded The Giving Pledge — a campaign to encourage the world’s wealthiest people to commit the majority of their wealth to philanthropy. As of 2025, over 240 billionaires from around the world have signed the pledge.

The pledge is not legally binding — it’s a moral commitment, a public promise. Critics have noted that some pledgers have been slow to follow through, and that pledging to give “the majority” of a fortune that keeps growing can mean the actual giving never catches up to the growing. Fair points. But the cultural shift the Giving Pledge represents — normalizing the idea that extreme wealth carries extreme obligation — is significant.

What About the Kids?

Buffett’s three children — Susan (Susie), Howard, and Peter — will each inherit a foundation to run, but they won’t receive huge personal windfalls. Buffett has said he wants to leave his kids “enough money so that they would feel they could do anything, but not so much that they would feel like doing nothing.”

Howard Buffett runs a foundation focused on global food security. Peter Buffett is a musician and philanthropist. Susan Buffett focuses on education. None of them live like heirs to a $140 billion fortune. By Buffett’s design, they don’t get to.

“I want to give my kids just enough so that they would feel that they could do anything, but not so much that they would feel like doing nothing.” — Warren Buffett

📊 Chapter 12: The Numbers — What Berkshire Actually Is

Let’s zoom out and look at what Warren Buffett has actually built, because the scale of Berkshire Hathaway is genuinely hard to comprehend.

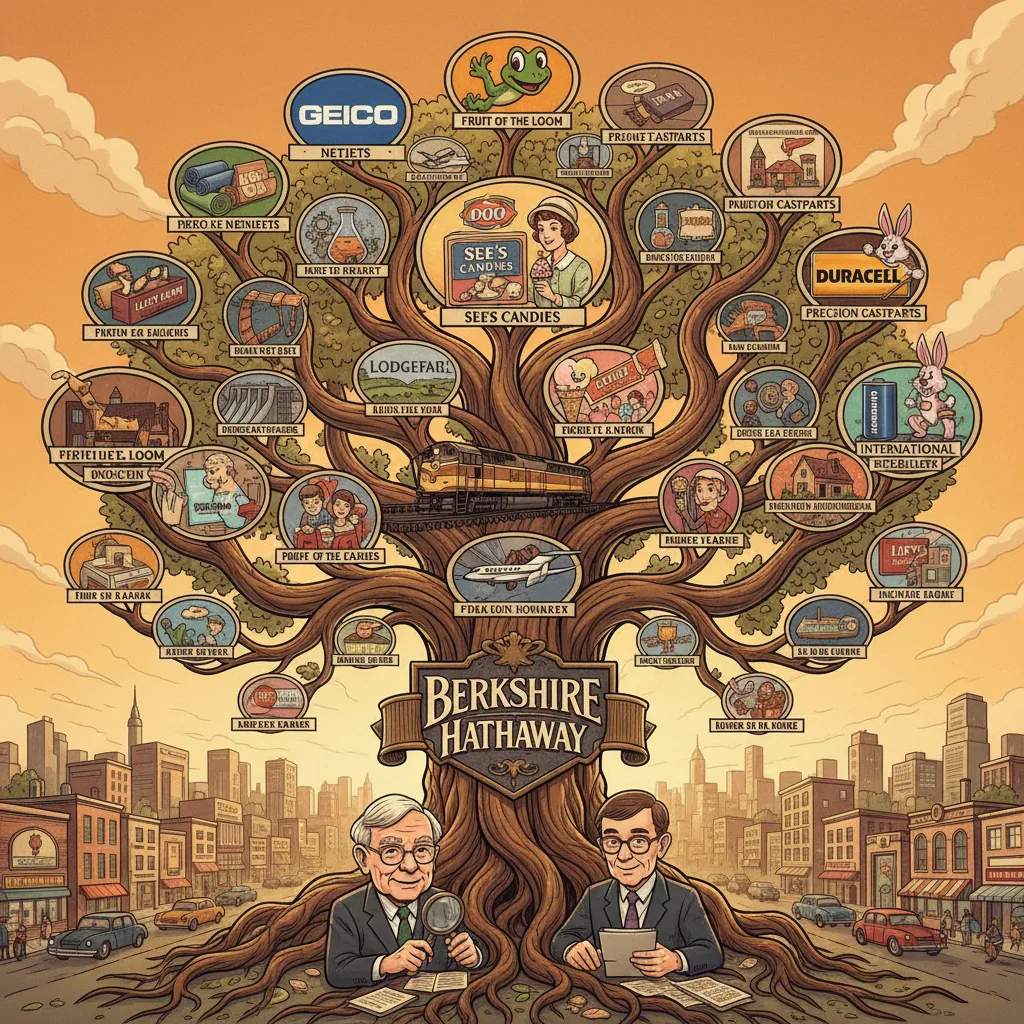

The Conglomerate

Berkshire Hathaway is not a hedge fund. It’s not a holding company in the traditional sense. It’s a sprawling conglomerate that fully owns over eighty operating businesses and holds massive equity positions in dozens more. Here’s a partial list of what Berkshire owns outright:

- GEICO — one of the largest auto insurers in the U.S.

- BNSF Railway — one of the largest freight railroads in North America

- Berkshire Hathaway Energy — a massive utility company

- Precision Castparts — aerospace and industrial components

- Lubrizol — specialty chemicals

- See’s Candies — premium chocolates

- Dairy Queen — ice cream and fast food

- Duracell — batteries

- Fruit of the Loom — underwear and apparel

- Benjamin Moore — paints

- Nebraska Furniture Mart — the largest furniture store in the U.S.

- FlightSafety International — pilot training

- International Metalworking Companies (IMC) — cutting tools

- Brooks Running — athletic shoes

And that’s not even half the list. Berkshire also holds massive stock positions in Apple, Coca-Cola, American Express, Bank of America, Chevron, Occidental Petroleum, and many others.

The Numbers

As of early 2026:

- Market capitalization: Over $900 billion

- Revenue: Over $360 billion annually — more than most countries’ GDP

- Cash on hand: Over $300 billion — a historic record that has prompted endless speculation about what Buffett plans to do with it

- Employees: Over 380,000 across all subsidiaries

- Class A share price: Over $600,000 per share — the most expensive stock on any major exchange, anywhere in the world, ever

That share price isn’t a typo. Buffett has never split Berkshire’s Class A stock. His reasoning: splitting attracts short-term traders, and he wants long-term owners. If you can’t afford a $600,000 share, he created Class B shares in 1996 (currently around $400) for smaller investors. But the Class A shares remain a monument to Buffett’s stubborn refusal to play Wall Street’s games.

The Management Philosophy

Berkshire’s corporate headquarters has roughly thirty employees. Not three hundred. Not three thousand. Thirty. For a company with $360 billion in revenue and 380,000 employees. There is no HR department. No legal department. No investor relations team. No strategic planning division.

Buffett’s management philosophy is radical decentralization. He buys great businesses, keeps the existing management in place, and leaves them alone. He doesn’t send consultants. He doesn’t impose standardized processes. He doesn’t hold quarterly strategy reviews. He allocates capital and lets his managers run their businesses.

His one ask: send him the excess cash. That’s it. Each subsidiary operates independently, and Buffett takes the cash they generate and reinvests it wherever he sees the best opportunity. The CEOs of Berkshire’s subsidiaries reportedly love working for Buffett because he gives them something almost no other corporate parent does: freedom.

“We delegate to the point of abdication.” — Warren Buffett

👑 Chapter 13: The Oracle at Ninety-Five — Legacy and the Long Goodbye

As of March 2026, Warren Edward Buffett is ninety-five years old. He still goes to the office nearly every day. He still reads for five to six hours a day — financial statements, newspapers, magazines, and books. He still drinks his Cherry Cokes. He still eats his McDonald’s. And he still controls, from a modest office in Omaha with no computer on his desk, one of the largest and most valuable companies on Earth.

What He Represents

There’s something almost mythological about Buffett at this point. In an era of tech billionaires who made their fortunes in a decade, Buffett built his over seven decades. In a world of algorithmic trading and AI-driven portfolios, Buffett reads paper annual reports and thinks. In a culture that celebrates disruption and “moving fast and breaking things,” Buffett buys and holds and does nothing.

He represents a set of values that feel almost antiquated: patience, discipline, intellectual honesty, frugality, and the radical idea that you don’t need to be flashy, loud, or cruel to build something extraordinary.

The Contradictions

But let’s not canonize the guy. Buffett’s Berkshire has faced legitimate criticisms. His insurance companies, like all insurance companies, have been accused of fighting legitimate claims to protect margins. His investment in Coca-Cola has supported a company whose products contribute to obesity and diabetes worldwide. His cozy relationships with Wall Street banks have raised questions about whether the Oracle has been as independent as he claims. His slow response to the Wells Fargo scandal suggested that even Buffett can be blinded by financial interest.

And there’s the broader question that hangs over all billionaire philanthropy: if your system of capital allocation is so brilliant that you can amass $140 billion in personal wealth, maybe the system itself is the problem. Buffett himself has said the tax code is broken — famously noting that his secretary pays a higher tax rate than he does. But he hasn’t exactly led a crusade to change it.

The Letters Will Remain

When Buffett is gone — and at ninety-five, that reality is closer than anyone likes to think about — what he’ll leave behind isn’t just Berkshire Hathaway. It’s sixty years of annual letters that read like a correspondence course in business, investing, and clear thinking. It’s a philosophy of investing that has been copied by thousands of fund managers worldwide. It’s the Giving Pledge, which may ultimately redirect hundreds of billions toward human welfare. And it’s a model of leadership that says you can be the most successful capitalist in history while eating McDonald’s for breakfast and driving yourself to work.

Is Warren Buffett a saint? No. Is he a genius? Probably. Is he the greatest investor who ever lived? By any quantitative measure, almost certainly yes.

But here’s what makes the story enduring: it’s not really about investing. It’s about a kid in Omaha who found the thing he loved, got better at it every single day for eighty years, and never stopped. He found his snowball at the top of a very long hill, and he pushed it — patiently, methodically, joyfully — until it became an avalanche.

“Life is like a snowball. All you need is wet snow and a really long hill.” — Warren Buffett

The hill is still going.

📅 Timeline

| Year | Age | Event |

|---|---|---|

| 1930 | 0 | Born in Omaha, Nebraska, during the Great Depression |

| 1936 | 6 | Buys six-packs of Coca-Cola and sells individual bottles door to door |

| 1941 | 11 | Buys first stock — three shares of Cities Service Preferred at $38/share |

| 1943 | 13 | Files first tax return; reportedly deducts his bicycle as a business expense |

| 1944 | 14 | Running five paper routes simultaneously; earning $175/month |

| 1945 | 15 | Buys a 40-acre farm in Nebraska with paper route savings for $1,200 |

| 1947 | 17 | Launches pinball machine business with friend Don Danly |

| 1949 | 19 | Graduates from University of Nebraska; rejected by Harvard Business School |

| 1950 | 20 | Enrolls at Columbia Business School to study under Benjamin Graham |

| 1951 | 21 | Graduates from Columbia; visits GEICO headquarters on a Saturday |

| 1952 | 22 | Marries Susan Thompson |

| 1954 | 24 | Goes to work for Benjamin Graham at Graham-Newman Corp. in New York |

| 1956 | 25 | Returns to Omaha; starts Buffett Partnership with $105,100 |

| 1962 | 32 | Begins buying Berkshire Hathaway shares at ~$7.50/share |

| 1965 | 35 | Takes control of Berkshire Hathaway; becomes chairman |

| 1967 | 37 | Buys National Indemnity insurance company for $8.6M — the float strategy begins |

| 1969 | 39 | Closes partnerships after 13 years with zero losing years; personal wealth ~$25M |

| 1972 | 42 | Buys See’s Candies for $25M with Charlie Munger |

| 1973 | 43 | Invests $10M in The Washington Post Company |

| 1977 | 47 | Susan Buffett moves to San Francisco; Astrid Menks enters his life |

| 1988 | 58 | Begins buying Coca-Cola stock; eventually invests $1.3B for ~7% of the company |

| 1996 | 66 | Buys remainder of GEICO for $2.3B; creates Berkshire Class B shares |

| 1998 | 68 | Acquires Dairy Queen for $585M; acquires General Re for $22B |

| 2004 | 74 | Susan Buffett dies of cancer |

| 2006 | 76 | Pledges ~$37B to Gates Foundation — largest charitable gift in history; marries Astrid Menks |

| 2007 | 77 | Makes $1M bet that an index fund will beat hedge funds over 10 years |

| 2008 | 78 | Invests billions during financial crisis — Goldman Sachs, GE, Bank of America |

| 2010 | 80 | Berkshire acquires BNSF Railway for $44B; co-founds The Giving Pledge with Bill Gates |

| 2016 | 86 | Begins buying Apple stock — eventually accumulates ~$36B position |

| 2017 | 87 | Wins the $1M hedge fund bet decisively; S&P 500 returns 125.8% vs. hedge funds’ ~36% |

| 2018 | 88 | Berkshire’s Apple position becomes its single largest equity holding |

| 2023 | 93 | Charlie Munger dies at age 99 on November 28 |

| 2024 | 94 | Designates Greg Abel as successor; begins trimming Apple position; cash reserves hit record levels |

| 2025 | 95 | Berkshire market cap exceeds $900B; cash hoard surpasses $300B; lifetime charitable giving exceeds $55B |

💡 Key Insights

- ▸ Buffett bought his first stock at age eleven and sold it after a small gain — missing a massive run-up. That single childhood mistake taught him the foundational lesson of his entire career: patience is the most valuable commodity in investing, and most people sell too early because they can't tolerate discomfort.

- ▸ When Buffett was rejected by Harvard Business School, he discovered that Benjamin Graham — the father of value investing — taught at Columbia. That rejection redirected him toward the single most important intellectual mentorship of his life. The best things that happen to you are often disguised as failures.

- ▸ Berkshire Hathaway was originally a failing textile mill that Buffett bought out of spite after the CEO tried to lowball him on a share tender. He turned it into a $900B+ conglomerate — but he's called the original purchase 'the dumbest stock I ever bought.' Even legends make mistakes. The key is what you build on top of them.

- ▸ Buffett's most powerful investment insight is deceptively simple: buy wonderful companies at fair prices, then do absolutely nothing. His largest holdings — Coca-Cola, Apple, American Express — were purchased years or decades ago and simply left alone. In a world addicted to action, inaction is his edge.

- ▸ Despite accumulating over $100 billion in personal wealth, Buffett has pledged to give away 99% of it and still lives in the same house he bought in 1958. He eats McDonald's for breakfast and drinks five Cherry Cokes a day. His frugality isn't performance — it's genuine indifference to the things money can buy, paired with a deep obsession with the game of making it.

Sources

- Alice Schroeder — The Snowball: Warren Buffett and the Business of Life ↗

- Berkshire Hathaway Annual Shareholder Letters (1965–2025) ↗

- Berkshire Hathaway SEC Filings ↗

- Roger Lowenstein — Buffett: The Making of an American Capitalist ↗

- Forbes Billionaires Index — Warren Buffett ↗

- Bloomberg Billionaires Index — Warren Buffett ↗

- HBO Documentary — Becoming Warren Buffett (2017) ↗